It can happen to pay the car tax late beyond the expected expiration date, but how much are the penalties and interest for late payment? How much time do I have to pay the motor vehicle tax, and especially what are the risks if I don’t pay the stamp duty before it goes on prescription?

Here we will see how to calculate penalties and interest for a late paid car tax. We anticipate that with regards to the sanctions a strong reduction is already foreseen, maximum at 5% thanks to the so-called “Industrious repentance” which allows for the regularization of the payments of the motor vehicle tax within three years. After this deadline, the increase of the amount with the 30% penalty plus daily tax interest.

Therefore, within the first two years, the increase in the amount to be paid for the expired stamp it is rather contained: “self-financing” by not paying the tax is a recommended operation only without going beyond the period in which repentance is in force. We deal with this topic relating to extension of the car tax deadlines foreseen in March, April and May.

Car tax redemption

With the repentance it is possible to regularize omitted or insufficient payments and other fiscal irregularities, benefiting from the reduction of penalties, including car tax (but also trucks, motorcycles, etc.): active repentance it was extended by two years with the conversion law of decree n. 124/2019 that is the Tax Decree 2020, thanks to which the news that the car tax can be paid within three years with penalty reduced to 5% instead of 30%.

How long do I have to pay the stamp duty with reduced penalties?

But how much time do i have to pay the car tax? If so forget to pay the stamp duty by the deadline what happens? Don’t worry if you pay it within two years you are still safe (or almost 😏).

In fact, after the first year, thanks to industrious repentance, you no longer have to pay the 30% stamp penalty (to which the interests tax), but instead passes to a 1/7 of the previous sanction, that is the 4.286%, plus daily interest.

This reduction of the sanction is applied only if the regularization of the stamp duty takes place within two years from non-payment.

After two years from the expiry of the stamp (but not more than three), in fact the penalty reaches 1/6, that is 5% plus daily interest.

Self-sanction stamp as it is calculated

These are the penalties for late payment to be added to the cost car tax:

👉 0.1% within 15 days beyond the deadline (quick repentance);

👉 + 1.5% from the 16th day and up to 30 days beyond the deadline (short repentance);

👉 + 1.67% from the 31st day and up to 90 days thereafter (average repentance);

👉 + 3.75% from the 91st day up to one year (long repentance); + 4.286% beyond the first year and up to the second (two-year repayment);

👉 + 5% beyond the first two years (more than two years repentance).

Car tax, interest and penalties as they are calculated for late payment

In all cases, in addition to the sanction, the cost of the daily legal interests shown below in the table where we see how penalties and legal interests are calculated in the context of active repentance. Over the years the percentages of penalties and interest have changed. For the sake of completeness, the table shows all of them in order to have a complete view. To be taken into consideration is the one referred to from 25/12/2019 for penalties and from 1/1/2020 for interest.

| SANCTIONS | ||||||

| Sanctions validity period | Ravved. rapid (within 15 days) |

Ravved. short (in 30 days) |

Ravved. medium (within 90 days) |

Ravved. long (within a year) |

Ravved. biennial |

Ravved. within 3 years |

| Until 28/11/2008 | – | 3.75% | – | 6% | ||

| From 29/11/2008 to 31/01/2011 | – | 2.5% | – | 3% | ||

| From 01/02/2011 | – | 3% | – | 3.75% | ||

| From 06/07/2011 | 0.2% per day | 3% | 3.75% | |||

| From 01/01/2015 | 0.2% per day | 3% | 3.33% | 3.75% | ||

| From 01/01/2016 | 0.1% per day | 1.5% | 1.67% | 3.75% | ||

| From 25/12/2019 | 0.1% per day |

1.5% | 1.67% | 3.75% | 4.286% | 5% |

| INTERESTS | ||||||

| Period of validity of legal interests | INTEREST Annual rate | |||||

| From 01/01/2004 to 31/12/2007 | 2.5% | |||||

| From 01/01/2008 to 31/12/2009 | 3% | |||||

| From 01/01/2010 to 31/12/2010 | 1% | |||||

| From 01/01/2011 to 31/12/2011 | 1.5% | |||||

| From 01/01/2012 to 31/12/2013 | 2.5% | |||||

| From 01/01/2014 to 31/12/2014 | 1% | |||||

| From 01/01/2015 to 31/12/2015 | 0.5% | |||||

| From 01/01/2016 to 31/12/2016 | 0.2% | |||||

| From 01/01/2017 to 31/12/2017 | 0.1% | |||||

| From 01/01/2018 to 31/12/2018 | 0.3% | |||||

| From 01/01/2019 to 31/12/2019 | 0.8% | |||||

| From 01/01/2020 | 0.05% |

Effective repentance within two years, a practical example of how much more interest and penalties I pay

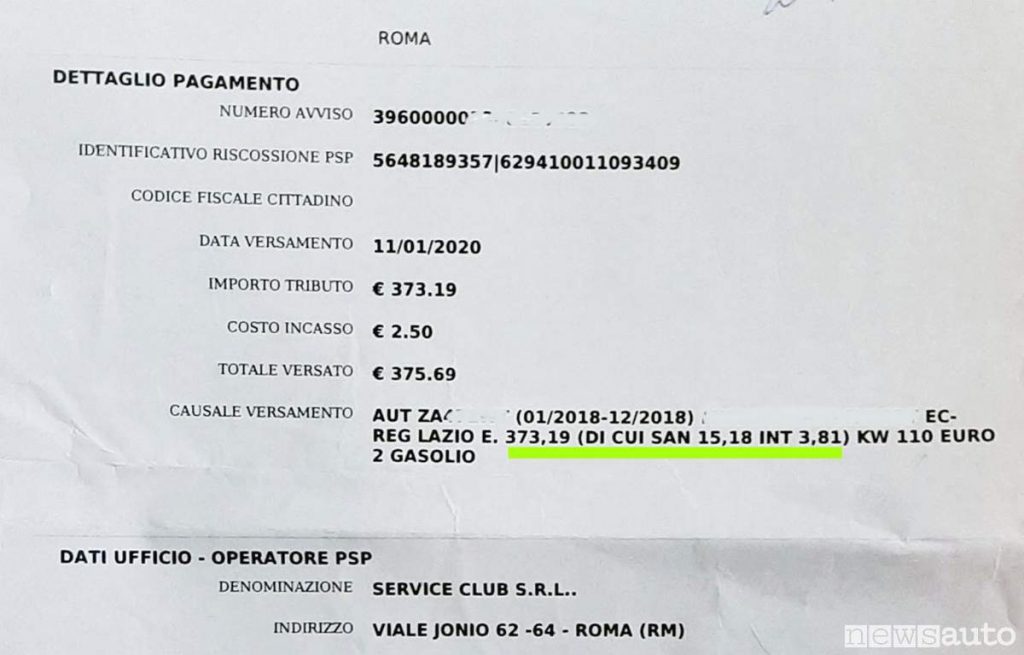

To example for a stamp duty of € 354.20 expiring a December 2018 and paid to January 2020 2 years late (natural deadline by 31 January 2018): the reduced penalty it is calculated by multiplying 354.20 by 4.286% or € 15.18, while the interest amounts to € 3.81.

The total paid amounts to 373.19 plus 2.50 of the cost of collection provided at the ACI counter: the actual cost to “finance” the 354 euros using the shock absorber of the car tax was exactly € 18.99.

See details of receipt for payment of the stamp duty made with a 2-year delay made at an ACI counter.

thanks to industrious repentance. In this case, a 2018 stamp duty expiring on 31/01/2018 and paid on 11/1/2020, 2 years later.

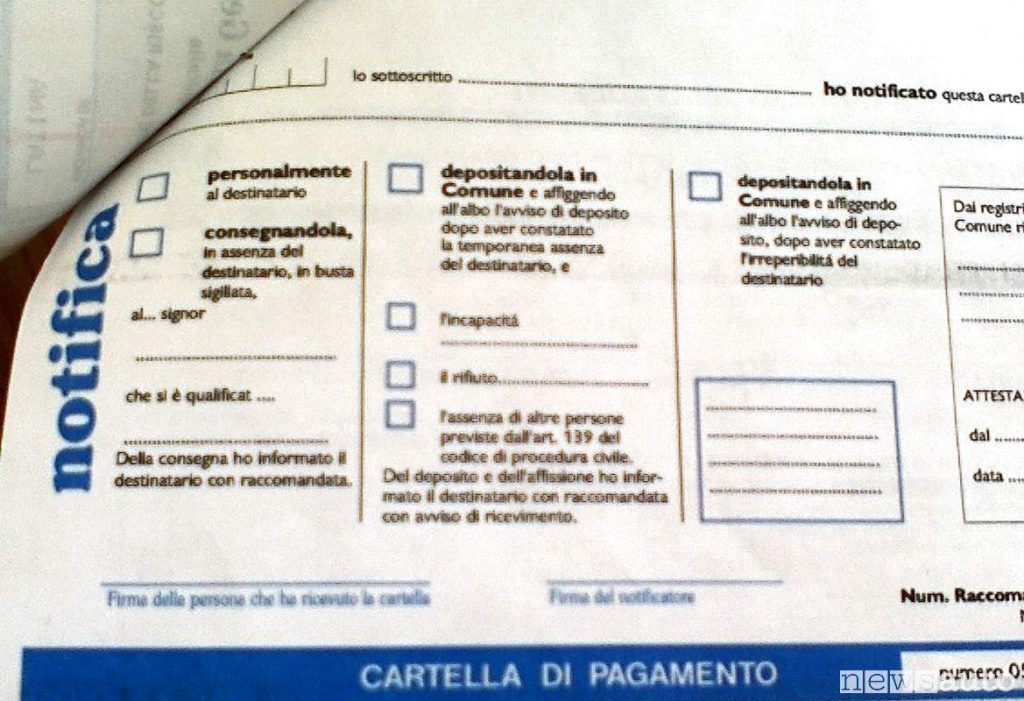

Tax bill for car tax, notification

However the active repentance is applicable only within two years in which theRevenue Agency and has not been notified the tax notice that, I recall, it is an act of order to pay, a notice of default addressed to the taxpaying citizen with which theRevenue-Collection Agency asks not only for payment but will subsequently activate for the compulsory recovery of this amount if it is not paid, regularized, within the established dates. This notice of payment of the car tax can be notified in two ways: classic tax notice, (registered with acknowledgment of receipt or in judicial documents) or through PEC.

by the Revenue-Collection Agency

Regional ownership tax car stamp

While remembering that the car tax is a regional tax to be paid on its regular due date even if the car is not in circulation. In fact, it is enough simply to be the owner of the vehicle to trigger the obligation to pay this vehicle tax since it is transformed from a road tax to a possession tax.

Stamp duty is a possession tax of the cars established with Presidential Decree of 5 February 1953 n. 39 (“Consolidated text of motor vehicle tax laws“). L’article 7 of law n. 99 of 23 July 2009 modified paragraph 29 of article 5 of Legislative Decree no. 953 of 1982, providing for the assignment to the tax for all those who appear to be for a vehicle owners, usufructuaries, buyers with retention of title, or users by way of financial leasing, from the Public Automobile Registry (PRA).

What happens if I don’t pay the road tax?

What if I don’t pay? Beware, if you exceed three years of failure to pay the stamp duty you risk the car ex officio cancellation of the vehicle from the PRA archives by the Region of belonging.

If you circulate after the cancellation of the PRA you risk the seizure and confiscation of the vehicle, but also a fine from 419 to 1682 euros.

Prescription for payment of stamp duty

If, within three years from the expiry of the stamp, a notification of assessment is not received, the payment is time barred, but in some cases it is necessary to appeal.

VADEMECUM CAR STAMP

Car tax notice Stay up to date on all the news of the car tax from our section dedicated to updates on the car tax.

💥 I notify: to stay up to date on everything and receive the latest news from the automotive world periodically on your email subscribe to the automatic Newsauto newsletter HERE

👉 Leave a comment on the speech stamps & surroundings on the FORUM!

COMMENT WITH FACEBOOK

#Car #tax #paid #late #penalty #interest #reduced