Like all potentially devastating changes, this one started off low-key. On the night of Wednesday (26), the managers of the Maxi Renda real estate fund, from BTG Pactual, released a material fact. They informed the approximately 490 thousand shareholders of the fund, the most popular in the market, that the Securities and Exchange Commission (CVM) had determined a change in the calculation of the amount of the dividend that could be distributed. The implications were potentially huge and could undermine the main attraction of these funds, which is the regular payment of monthly tax-free dividends, a facility that has attracted 1.5 million Brazilians in the last two years.

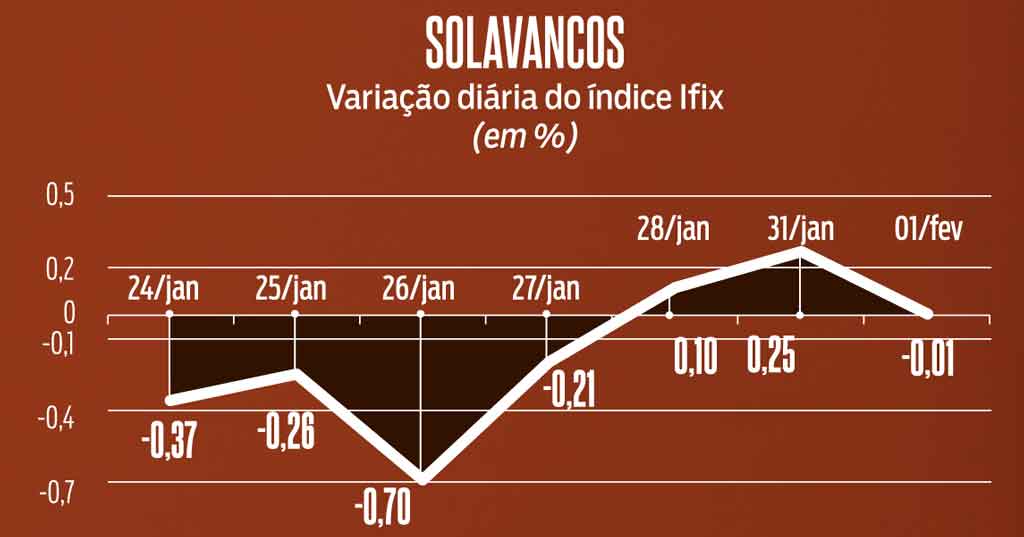

In response to a request from BTG on Tuesday (1), the CVM temporarily suspended the effect of the decision. Managers will now have 15 days to defend the non-implementation of the change. Meanwhile, the traditionally stable Ifix index, which gathers the most traded real estate funds on the B3, showed unusual bumps (see chart). And there should still be more volatility in the coming days, as managers are forced (or not) to adapt to the new rule.

“The CVM’s intention was to prevent managers from distributing dividends when funds have accounting losses, but this caused enormous uncertainty” Raphael Pires partner at Candido Martins Advogados

The market scare occurred because the CVM rewrote its own decision, published in 2014. At that time, the Commission established clear parameters for investor remuneration. It is mandatory to distribute at least 95% of the profits. The remaining 5% is intended to cover the fund’s costs, including the remuneration of the manager (who makes investment decisions) and the administrator (who controls the inflow and outflow of funds and the purchase and sale of real estate assets). All very simple. Until the CVM itself asked a few days ago: when the manager says “profit”, what is he talking about?

CASH AND COMPETENCE Let’s explain the problem with an example. Suppose a real estate fund has only one asset, a logistics warehouse worth R$100 million. The property was leased for ten years for R$ 1 million per month. If the fund doesn’t spend anything on maintenance, it’s all profit. And it will be possible to pay R$ 950 thousand per month to shareholders.

So far, everything is very clear. However, accounting standards require the owner to “devalue” his property by 10% every year, the so-called depreciation. Thus, each year there will be an accounting “loss” of R$ 10 million, which has nothing to do with the market value of the property or the rent paid by the tenant. In other words, there will be a monthly accounting “expense” of R$ 833 thousand, almost 90% of the amount allocated monthly to shareholders. What is the correct profit: BRL 950,000 (the rent amount) or BRL 117,000 (the rent minus the depreciation)? Under the cash basis, it is R$ 950 thousand. Under the accrual basis, it is R$ 117 thousand.

The turmoil was caused by the fact that, in the 2014 decision, the CVM determined that profit should be calculated on a cash basis. Now, the determination, whose application has been temporarily suspended, is that the calculation be made on the accrual basis. “The CVM’s intention was to prevent managers from distributing dividends even if the funds showed accounting losses, but this caused enormous uncertainty,” said lawyer specializing in real estate funds Raphael Pires, a partner at Candido Martins Advogados. And the depreciation is just one point. There are dozens of other variables and accounting criteria that today are simply not considered by managers when calculating how much to pay the investor, and which they may now have to enter into this account.

By changing the calculation, the CVM may prevent funds with physical assets, called “bricks”, from distributing monthly returns on a regular basis. Managers may be required to recognize depreciation expenses, which are calculated twice a year, and begin to pay compensation every six months. The impact can also be intense on funds of funds, which pool shares in various portfolios to reduce risk. By depending on the results of other portfolios, managers may have to make provisions for future accounting losses, changing the payment mechanics that are so pleasing to the investor.

Although the decision announced on January 26 only refers to the Maxi Renda fund, in a subsequent statement the CVM warned that the understanding “may be applied to other cases”. Those who know the industry estimate that there will be weeping, gnashing of teeth and discreet pressure. “Much of the growth in real estate funds was due to retail banking products,” said a manager who preferred not to be named. “Big financial institutions and the construction sector itself, which is increasingly dependent on funds to sell their properties, are already preparing for a powerful lobby.” Wait for the scenes of the next chapters.

The post Cracked structure? appeared first on ISTOÉ DINHEIRO.

#Cracked #structure #MONEY