With inflation soaring and despite the fact that the US and the euro zone have not yet fully recovered from the consequences of the pandemic, central banks have begun to raise interest rates. As a consequence, the Euribor (the index to which almost 80% of variable mortgages in Spain are referenced) has returned to positive rates after six years in negative.

Specifically, the 12-month Euribor went negative in 2016, going from +0.042% in January to -0.008% in February, and registered its monthly historical low in January 2021 (-0.505%). It has not been until April of this 2022 when it has been seen again at positive levels. And in recent weeks the trend has accelerated, due to high inflation, aggravated by the Ukrainian war, and its impact on the accelerated monetary normalization by central banks. The Euribor closed August at 1.249% and on average for September it is already above 2% (2.059%).

This is leading almost all entities to raise the fixed interest rates they offer on mortgages, which generally already exceed 2.5% APR, while both the initial rates and the spreads they apply to variable mortgages are lowering.

And it is that the strategy of financial institutions is taking a 180 degree turn. In this context, the preference of users for the fixed rate is clear (80.56%) and mixed mortgages triple, which already account for 18.06%, according to a Trioteca report in August.

Banking, in general, has been making variable mortgages cheaper to increase hiring and take advantage of the increase in the Euribor, which now improves bank margins. The differentials that are added to the Euribor are already down 0.8% in entities such as Evo Banco, Pibank, Kutxabank, Ibercaja, Coinc and Bankinter.

“The value of the Euribor has skyrocketed and is already in positive values, something that has not happened for six years. Banks such as Coinc, BBVA and Bankinter have lowered their variable rates to compensate for this rise and attract more customers. This is great news for those looking to contract a variable mortgage. Although it is important to bear in mind that if the Euribor continues to rise as all the experts predict, the mortgaged party will pay much more expensive installments each time the mortgage is reviewed (half-yearly or annually), “they explain since HelpMyCash.

Best prices

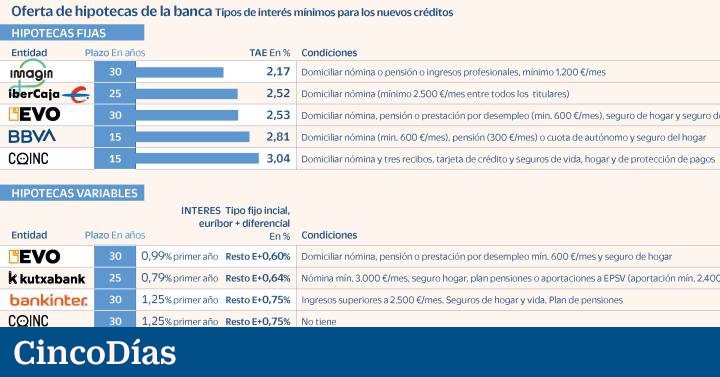

The smart mortgage EVO Bench is one of more best variable mortgages on the market, according to the financial comparator HelpMyCashsince it has a low interest rate of 0.99% the first year and Euribor plus a spread of 0.60% the rest, well below the average, which is Euribor plus 0.85%.

This interest, in addition, is discounted for contracting few products or services of the entity: recurring income of at least 600 euros per month and subscribing to your home insurance. If none of these requirements are met, the rate rises to 1.19% the first year and to Euribor plus 0.80% for the following years.

A Euribor plus 0.64% offers the variable mortgage of Kutxabank, but it has more conditions if you want to achieve this differential. In addition to a minimum income of 3,000 euros, it is necessary to take out home insurance and make contributions to pension plans.

Among the cheapest variables, mortgages of Bankinter Y Coinc with 0.75% plus Euribor from the second year. The fixed rate for the first 12 months is 1.25%. That of Coinc does not require conditions, while that of Bankinter requires contracting home insurance, a pension plan and a minimum income of more than 2,500 euros per month.

Among the fixed-rate mortgages, with an APR of less than 2.5%, there is only that of Imagin (CaixaBank’s mobile bank) which has 2.17% and as the only requirement to domicile the payroll, pension or minimum professional income of 1,200 euros per month. With 2.52% and 2.53% APR, the loans for home purchase from Ibercaja and EVO Banco stand out for 25 and 30 years, respectively. BBVA sells a 2.81% APR fulfilling conditions and Coinc exceeds 3% APR.

#offer #fixed #variable #rate #mortgages