Crises, like joys, are seen with different eyes depending on who is the passive subject. And this is one of those silent shocks, a blind spot in the wide angle of the world economy. Far from the headlines, the rise in interest rates is taking its toll on emerging and developing countries: last year the global south paid more for its debt – repayment of principal and interest – than it received in development aid and new loans. Money arrivals to this group of nations fell, in fact, to their lowest level since the global financial crisis, according to the figures from the NGO ONE Campaign. An alarm signal that should make the Federal Reserve and the European Central Bank (ECB) think.

In 2022, the first year of strong rate increases to curb rising inflation, countries in the Global South paid almost $50 billion (€46 billion) more in debt than they received in new financing, according to data of the UN trade and development arm (Unctad). In parallel, official development aid added its second consecutive annual drop and continued well below the objective of 0.7% of gross national income. A goal that dates back to the seventies of the last century and that, more than 50 years later, remains unfulfilled.

We are seeing a worrying trend: financial flows are leaving the developing countries that need them most and flowing to their creditors

Rebeca Grynspan, head of the UN trade and development arm (Unctad)

“We are witnessing a worrying trend: financial flows leave the developing countries that need them most and flow towards their creditors,” summarizes the head of Unctad, Rebeca Grynspan, in statements to EL PAÍS. “They are nations that need external resources to complement their internal efforts and, without a positive trend in external financing, their capacity for growth is severely limited.” The fiscal restrictions imposed by this situation, she adds, make both the Sustainable Development Goals (SDGs) almost impossible to achieve: “Addressing overlapping crises, such as the climate emergency, will be an unattainable challenge if these trends are not reversed.”

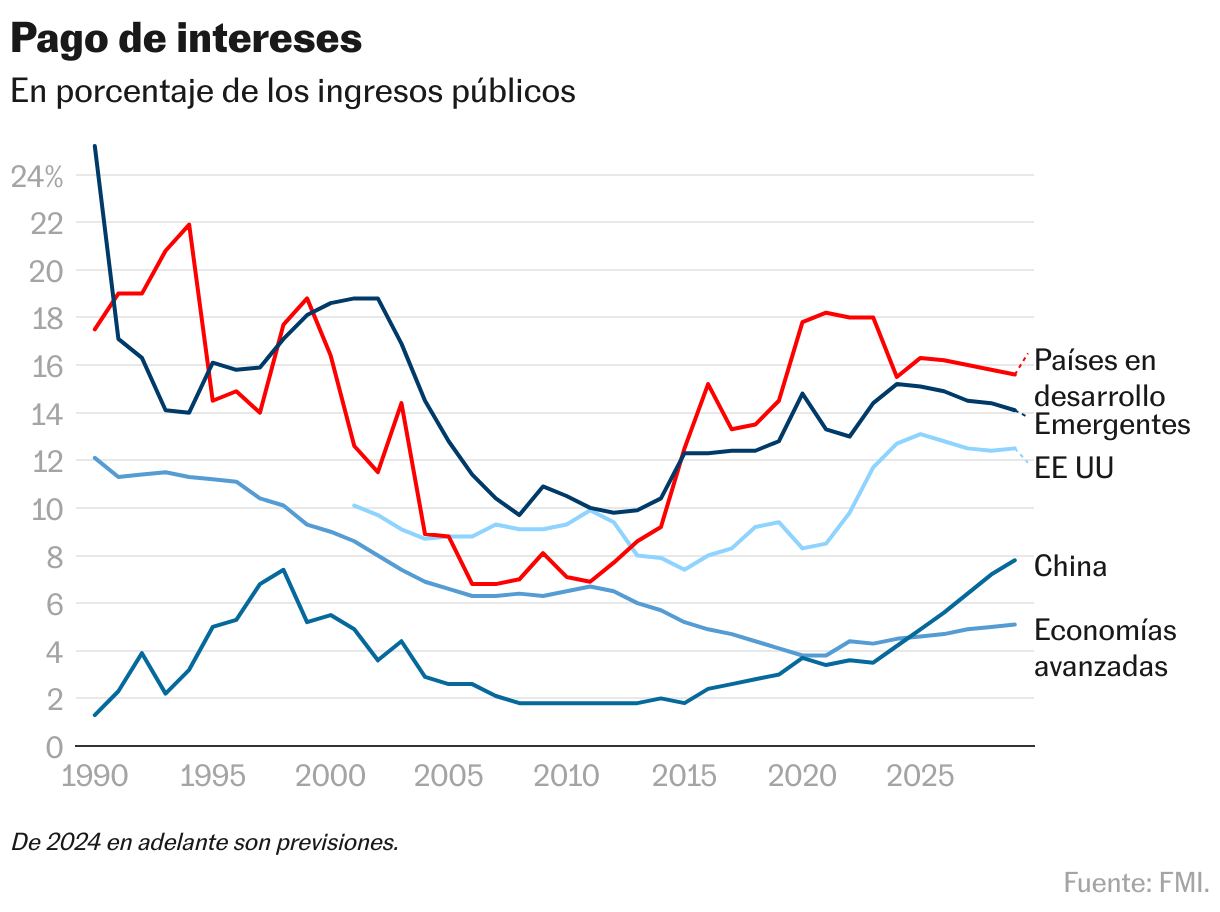

A reality that the International Monetary Fund (IMF) also recognizes in its latest fiscal monitor: “Many low-income countries continue to experience significant shocks.” The lender of last resort also points to the strong dollar as a key factor behind the increase in the cost of its debts; denominated, to a large extent, in that currency. And to the aid flows and financing from China, which have been falling for “several years.” Result: forced austerity with serious social consequences.

“It is said that there is no debt crisis in the sense that there is no crisis of the creditors, of the banks, which are better than ever,” outlines Juan Carlos Moreno-Brid, professor at the National Autonomous University of Mexico (UNAM). ) specialized in development economics. “But those who live in middle-income and, above all, low-income countries: they only see one reality: that of public investment, education and health clearly going down. “It is a silent crisis, but it is a debt crisis after all.” A crisis, he says, “with the face of the poor… and of the middle class of many emerging countries.”

Some time ago, since the very beginning of globalization and large-scale financing, the decisions of Washington and Frankfurt ceased to matter only to their area of influence. Today, that sphere is global: what is decided in the governing councils of the Fed and the ECB matters as much or more in Vilnius or Phoenix as in Nairobi or La Paz. “It is essential that the central banks of rich countries begin to lower rates soon,” cries Moreno-Brid because that will give room for emerging countries to also lower rates without the risk of capital flight. High rates, he adds, “aggravate” the problem of credit restriction for investing.

“The highest interest is hitting the emerging world more than the rest,” he acknowledges. Martin Castellano, of the Institute of International Finance (IIF, a kind of global banking association). “And, even more so, to the poorest countries, which have been expelled from the capital markets or which, in the best of cases, have had to tolerate higher funding costs.”

Africa, in the eye of the hurricane

The storm has settled, above all, on Africa. Although at the beginning of the year several of its countries were able to return to international debt markets after almost two years of forced absence, four of them – Ethiopia, Ghana, Zambia and Malawi – have already formally accepted the debt relief initiative. debt launched in the middle of the pandemic by the G20. Others, like Tunisia or Egypt, are also in serious trouble.

Aside from the most obvious – the higher payments derived from rate increases – there is an additional reality that makes things even more difficult for the region: half of its debt is multilateral in nature and, therefore, very difficult renegotiation. That does, according to a recent report by The Economist Intelligence Unitthat “other creditors, those who would have to absorb greater losses to restore debt sustainability [de estos países]resist participating in relief schemes.”

Nothing better than a bit of historical perspective: in 2000, recalls the Secretary General of Unctad, sub-Saharan Africa’s external debt was around 53% of its GDP, but debt service represented only 12% of exports. Today, its external debt is lower—41% of its GDP—but debt service represents 18% of its exports. The reason: the rise in interest rates. For the current financial year, the World Bank estimates that the costs associated with meeting public debt obligations will grow by 10% for all developing countries and almost 40% for low-income countries.

“When Africa spends more on interest than on education and Latin America spends more on interest than on public investment, we have to talk about a systemic failure,” Grynspan says. “A failure affects the lives of billions of people and it will take decades, not just years, to address its consequences if we do not find a debt restructuring mechanism that is effective and timely.”

Latin America, exception to the rule

In some respects, however, Latin America is also the other side. A region plagued by challenges and problems but in which, not so long ago, a rate rise like the attack on the northern bank of the Rio Grande would have unleashed a crisis of biblical proportions. Today is not like that: it is causing harm, yes, but it is far from being the feared apocalypse. “There are several factors that have alleviated the impact in the region: remittances [el dinero que envían los migrantes a sus familias] “They are at record levels, imports have decreased and exports have remained high…”, lists Castellano.

“All of this means that, even with an adverse monetary policy in the United States, several countries have achieved significant reductions in their current account deficits and in their need for external financing: they are only having to go out into the market taking advantage of opportunities and have even been able to increase the reserves,” adds the IIF technician. Although it has been languishing for years—the famous lost decade is already several, in the plural—Latin American GDP growth is holding up “better than expected.” Something that has also contributed, of course, to the rise in raw materials, of which several countries in the bloc are net exporters. An oasis in the always intricate emerging desert.

You can follow Future Planet in x, Facebook, instagram and TikTok and subscribe here to our newsletter.

#Global #South #pays #debt #receives #development #aid

{kind=link}