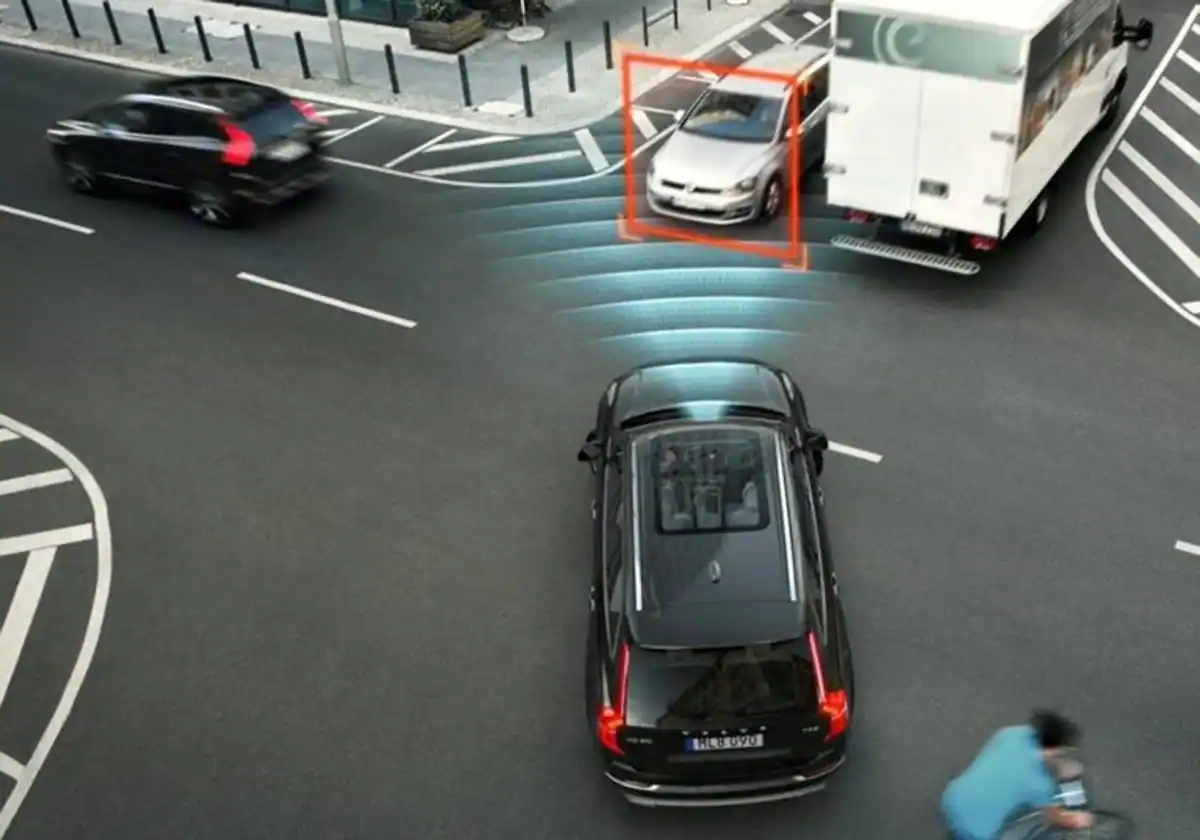

As of July 7, 2022, eight new driving assistance systems (ADAS) are mandatory in newly approved vehicles to improve the safety of the vehicle, its occupants and other users. And in July 2024 all new vehicles sold in the EU must already have these ADAS installed.

Also including a black box in the vehicle. Although it is not an ADA, it is a crash data storage and recording system that collects information from the vehicle and its occupants. In the event of an accident, it allows to know what happened before, during and after.

According to the DGT, different scientific studies support the effectiveness of ADAS. And they estimate that, if all vehicles match them, 40% of accidents, 37% of serious injuries and 29% of deaths would be prevented or mitigated. Therefore, if the expansion of ADAS leads to a reduction in the number of claims, repairs by insurance companies could be reduced in the coming years, which would lead to cheaper insurance; One could also speak of an increase in premiums, since repairing cars with these ADAS, with all their technology, will mean a higher cost. Thus, this balance between the reduction of claims and their severity and a higher cost of repairs, in what position does it place insurers? Will they lower or increase the premium?

Regarding an increase in the premium for the application of ADAS, Víctor López, head of insurance companies at Rastreator, qualifies that “there should not be large variations or changes. Precisely this new standard promotes the safety of drivers, so the insured will have less chance of suffering or causing an accident, which will not imply any new or extra cost that may lead to an increase in the price of their policy. In the only case that would mean an increase in the premium is if the infractions and, therefore, the fines increase, generating a greater number of people who appeal them. But this coverage must be contracted specifically, so it would not affect all policyholders. In the short term, it is not expected that there will be increases for this reason.

For Línea Directa Aseguradora, the policies will suffer an increase in price since repairs are more expensive. From Línea Directa they clarify that «it will depend on the accessory; there are some quite affordable and others less. And the more expensive and sophisticated a vehicle is, the more expensive it is to repair, but, a priori, it will also have fewer accidents. You have to keep in mind that when a technology becomes established and widespread, its price tends to decrease, which also influences its repair process.”

Antonio Guardiola, head of the UNESPA Technical Commission for Automobile Insurance, adds that “at the moment when technology evolves and is incorporated as a mandatory element in a vehicle, it allows a reduction in cost that implies less cost for the car, when acquiring it and when repairing it. We support any advance that translates into a reduction in road accidents, which implies fewer injuries. These systems entail a reduction in costs due to accidents and this reduction is transmitted in the price of the insurance. Each company will manage it as it sees fit, but most companies take it into account. It must be emphasized that we have a very aged fleet of cars (30%, between 15 and 20 years) and it is important to look for mechanisms for its renewal. It is useless to incorporate new ADAS if the park is old.

For Francisco Olmedo, director of Individuals at AXA Spain, “the price of the insurance is determined by a multitude of variables (type of driver, vehicle, use…), the incidence of which varies according to the coverage contracted. A higher-value, high-tech new vehicle may be more expensive for comprehensive coverage, although it may lower the price of coverages such as Civil Liability due to its more innovative security features. In any case, a safer vehicle that reduces the probability of having an accident will always have cheaper insurance.”

black box

The Black Box will help to elucidate the cause of the accident. Jesús Monclús (Fundación MAPFRE) qualifies that “it will make it possible to find out what really happened in the accident and, thanks to this, it will help research and improve vehicles and their safety systems and distribute responsibilities more fairly and with less uncertainty.” Thus, it will serve to reconstruct the accident (very useful information for insurance experts) and set the parameters for accident injuries.

Also including a black box in the vehicle. Although it is not an ADA, it is a crash data storage and recording system that collects information from the vehicle and its occupants. In the event of an accident, it allows to know what happened before, during and after.

According to the DGT, different scientific studies support the effectiveness of ADAS. And they estimate that, if all vehicles match them, 40% of accidents, 37% of serious injuries and 29% of deaths would be prevented or mitigated. Therefore, if the expansion of ADAS leads to a reduction in the number of claims, repairs by insurance companies could be reduced in the coming years, which would lead to cheaper insurance; One could also speak of an increase in premiums, since repairing cars with these ADAS, with all their technology, will mean a higher cost. Thus, this balance between the reduction of claims and their severity and a higher cost of repairs, in what position does it place insurers? Will they lower or increase the premium?

Regarding an increase in the premium for the application of ADAS, Víctor López, head of insurance companies at Rastreator, qualifies that “there should not be large variations or changes. Precisely this new standard promotes the safety of drivers, so the insured will have less chance of suffering or causing an accident, which will not imply any new or extra cost that may lead to an increase in the price of their policy. In the only case that would mean an increase in the premium is if the infractions and, therefore, the fines increase, generating a greater number of people who appeal them. But this coverage must be contracted specifically, so it would not affect all policyholders. In the short term, it is not expected that there will be increases for this reason.

For Línea Directa Aseguradora, the policies will suffer an increase in price since repairs are more expensive. From Línea Directa they clarify that «it will depend on the accessory; there are some quite affordable and others less. And the more expensive and sophisticated a vehicle is, the more expensive it is to repair, but, a priori, it will also have fewer accidents. You have to keep in mind that when a technology becomes established and widespread, its price tends to decrease, which also influences its repair process.”

Antonio Guardiola, head of the UNESPA Technical Commission for Automobile Insurance, adds that “at the moment when technology evolves and is incorporated as a mandatory element in a vehicle, it allows a reduction in cost that implies less cost for the car, when acquiring it and when repairing it. We support any advance that translates into a reduction in road accidents, which implies fewer injuries. These systems entail a reduction in costs due to accidents and this reduction is transmitted in the price of the insurance. Each company will manage it as it sees fit, but most companies take it into account. It must be emphasized that we have a very aged fleet of cars (30%, between 15 and 20 years) and it is important to look for mechanisms for its renewal. It is useless to incorporate new ADAS if the park is old.

For Francisco Olmedo, director of Individuals at AXA Spain, “the price of the insurance is determined by a multitude of variables (type of driver, vehicle, use…), the incidence of which varies according to the coverage contracted. A higher-value, high-tech new vehicle may be more expensive for comprehensive coverage, although it may lower the price of coverages such as Civil Liability due to its more innovative security features. In any case, a safer vehicle that reduces the probability of having an accident will always have cheaper insurance.”

black box

The Black Box will help to elucidate the cause of the accident. Jesús Monclús (Fundación MAPFRE) qualifies that “it will make it possible to find out what really happened in the accident and, thanks to this, it will help research and improve vehicles and their safety systems and distribute responsibilities more fairly and with less uncertainty.” Thus, it will serve to reconstruct the accident (very useful information for insurance experts) and set the parameters for accident injuries.

If the insurers can finally consult the information from the mandatory black boxes, the people who respond to the statistical profile will not experience either a higher or lower insurance premium and those who do not respond to what is expected of their profile will.

#insurance #price #ADAS #black #boxes #car #truth