They say that thinking big is good and those who bet on size are not wrong. Those who have seen unattainable prices in these values have been losing strong profits for years. Six companies are worth more than $ 1 trillion on the stock market – Microsoft ($ 2.4 trillion), Apple ($ 2.4 trillion), Aramco (2.01), Alphabet (1.94), Amazon (1.68) and Tesla (1.09) – and all of them have the American mark with the exception of the Saudi oil company Aramco.

In total, they capitalize 11.5 trillion dollars, a huge figure that is only surpassed by the Gross Domestic Product of the United States, which reached 20.94 trillion in the 2020 pandemic or 14.7 trillion in China. The aggregate capitalization of these six companies ranks as the equivalent of the world’s third largest economy, well ahead of Japan with a GDP of $ 5 trillion or Germany’s 3.8 trillion.

The comparison of this select group of companies with the respective Stock Exchanges of the aforementioned countries is also bleak. After Wall Street, which incorporates these cyclopes, the Japanese Topix index offers a market value of 3.9 trillion dollars and the EuroStoxx50 lags behind at 3.6 trillion, just twice that of the Parisian CAC and slightly more than the Dax. German. The whole of the Spanish Stock Exchange with Inditex as its flagship capitalizes 1,076 billion dollars and has been anchored in these figures for more than a decade.

With the exception of the oil company Aramco, which presents results on November 1, this week the business results of these giants have been released, with figures corresponding to a quarter that are dizzying: billings of more than 100,000 million dollars and colossal benefits. Except for Amazon and Apple, which have disappointed by not adjusting to what the market expected and show supply problems, the rest register growth in many activities more typical of small companies that are just starting out, with billing increases of over 40%.

The Wall Street giants that dominate technology, social networks and advertising are presented to many as an Orwellian Big Brother, with an unstoppable investment power and always under the continuous suspicion of the oligopoly, with anti-competitive practices. A success and control of their plots of activity that are also reflected in brutal profits, which they share with millions of shareholders. Also the numbers of workers are difficult to conceive. As an example, Amazon could end this last quarter of the year hiring 1.4 million workers.

Apple: Loose for chips and lose the throne due to capitalization

The Cupertino, California-based firm on Thursday announced results for the fourth quarter of its fiscal year that were lower than expected by market consensus. The sales with which Wall Street received the figures have caused Apple to lose the throne of the world market capitalization in favor of Microsoft, although the value of both is around 2.4 trillion dollars.

Apple obtained a profit in its fiscal year of 94,680 million dollars (81,422 million euros), 64.9% more. But he acknowledged the impact caused in the last quarter by the shortage problems of the production chain, as well as by the lack of chips, which amounts to 6,000 million dollars. Despite the uncertainty, Apple did point out that the next quarter will be one of “solid growth”, given the good reception from the market of the new i-phone 13.

Bankinter analysts explain that Apple has published revenue below market expectations for the first time since the first quarter of 2016. “Despite the logical negative reaction of the market in the short term, we continue to trust Apple’s potential in the medium term as a leader in its segment and due to the strong demand for products (especially the i-phone) and services ”, they indicate.

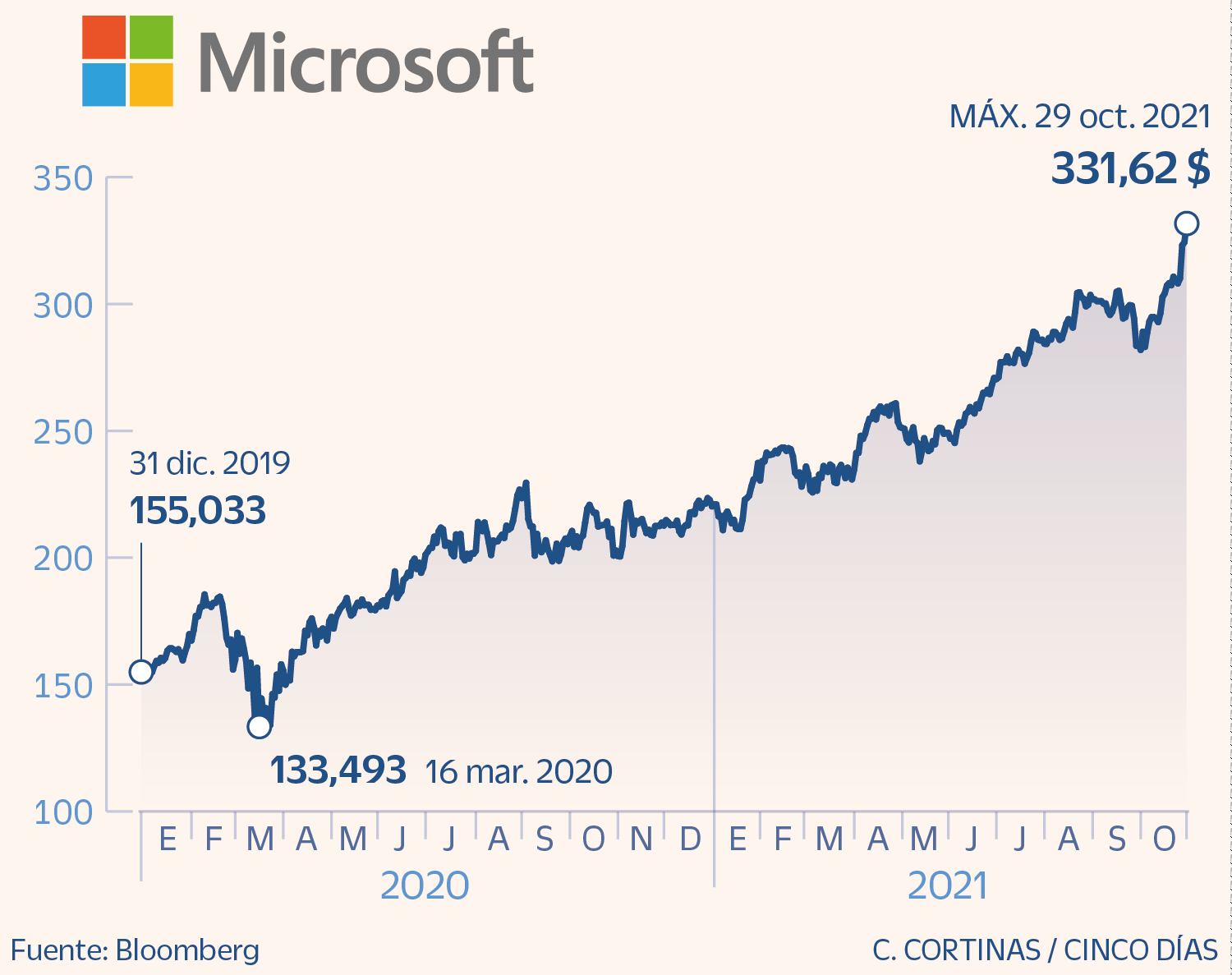

Microsoft: Starts its fiscal year powered by the ‘cloud’

The Redmond giant begins the first quarter of its fiscal year 2022 with net profits of 20,505 million dollars, which represents a growth of 48% compared to the previous quarter. Earnings that give wings to its market value of 2.46 trillion dollars, which makes it the most valuable company in the world on the stock market. Analysts have received these figures very well and indicate that “they are based on the strong evolution of the cloud business”, given the demand of companies that have adopted a hybrid model of teleworking. Revenues from this division reached $ 18.4 billion compared to a market consensus of $ 17.9 billion.

Goldman Sachs makes a very favorable reading of Microsoft and within 12 months it raises the target price of the share from 360 dollars to 400 dollars per share, which implies a potential of 23%. Goldman expects sustained double-digit growth along with continued margin expansion, particularly as the cloud business continues to gain weight in other activities. “Azure (the company’s cloud services division) has an increasing presence of large customers so we believe that Microsoft is well positioned to continue gaining market share,” they explain.

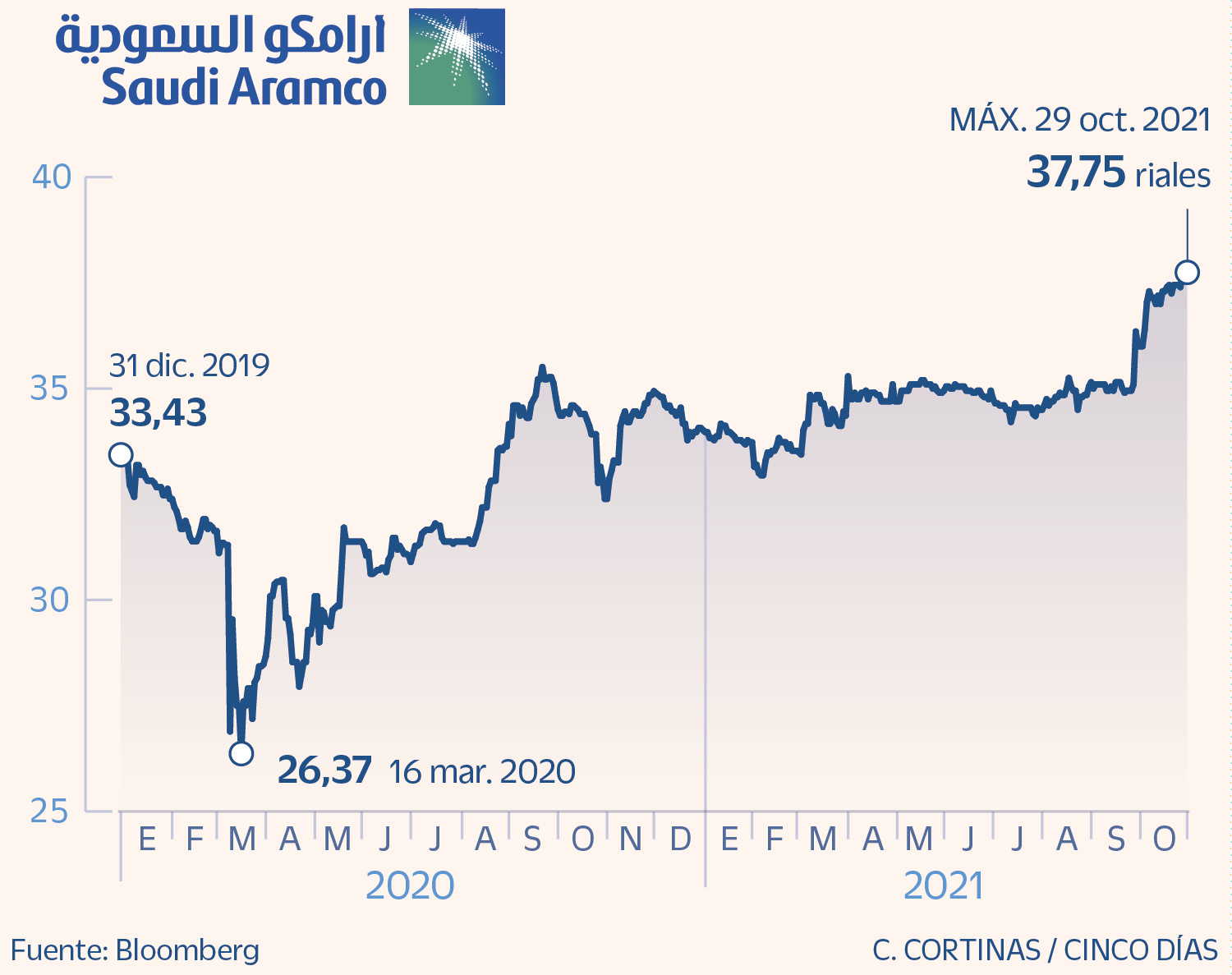

Aramco: On the sidelines of the sector’s favorites despite the rise in crude oil

The Saudi oil company Aramco, which capitalizes on the stock market 2.01 trillion dollars, has not quite convinced analysts. Next Monday it will release its third-quarter results, after skyrocketing in the second quarter to $ 25.3 billion. Results that should also be magnificent given the rise in oil prices, despite the increase in crude oil, it does not place it among the oil companies of choice for investors. Its strong cash generation is allowing it to reduce its indebtedness and Goldman Sachs analysts highlight the solidity of its balance sheet. However, they offer a neutral recommendation with a price target of 42 Saudi Riyals, up from 37.75 today. “We are neutral in the context of a positive view of the sector, as we find better combinations of valuation, high free cash flow and dividend yield in other parts of the sector.” Bank of America’s recommendation is also neutral, with a price target of 38 Saudi riyals. “Aramco’s current 4% dividend yield remains low globally. We firmly believe that the current and future trajectory of Aramco’s shares will depend on its ability to drive profitability for minority shareholders. “

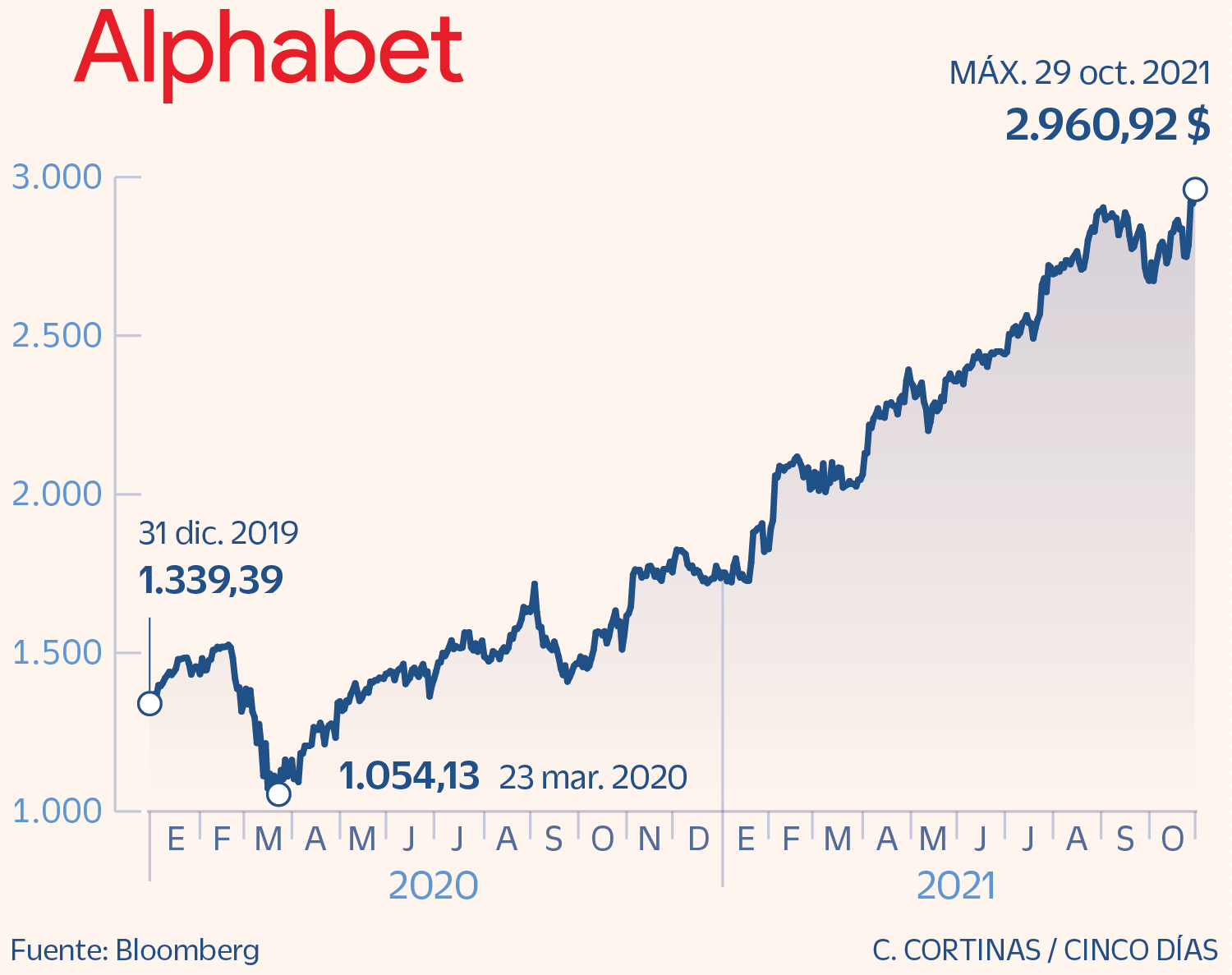

Alphabet: Surprise thanks to ad revenue

Alphabet (Google’s parent company) is steadily approaching a New York Stock Exchange value of $ 2 trillion. In the last twelve months, its shares have risen more than 80% and are already moving at levels of $ 2,900 per share. In mid-2019, the stock was moving at $ 1,065, drawing a bullish chart with hardly any stops. The results at the end of the quarter of this year accompany the optimism about the value. The company obtained profits of 55,391 million dollars (47,750 million euros) between January and September, more than double that in the same period last year. Bankinter analysts indicate that “the figures and growth presented confirm the enormous strength of the recovery of the advertising market and specifically the online segment, in which Alphabet generates close to 80% of its income”. Of course, YouTube and Google Cloud (cloud services) disappointed in terms of participation in the results. Goldman Sachs sets a price target of $ 3,350 due to “sustainable growth of advertising services; the growing contribution of Google Cloud as a multi-year investment cycle; expectations of growth in artificial intelligence, and profitability for shareholders ”, including share buybacks, they conclude.

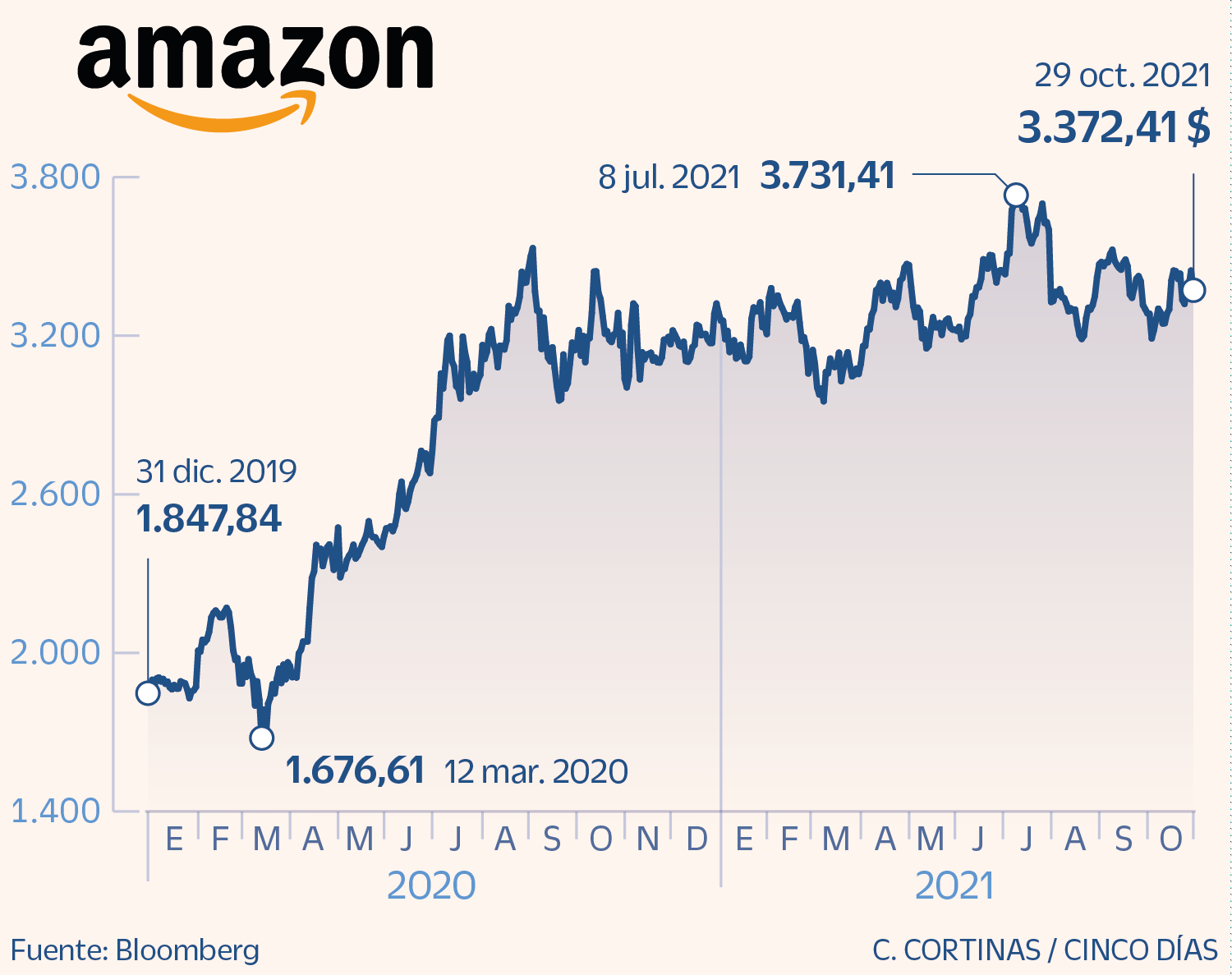

Amazon: The end of the postcovid pull and doubts about Christmas

Amazon’s turnover in the third quarter of the year reached 110,812 million dollars, 15% more year-on-year, and analysts expected a billion more, while Ebit stood at 4,852 million, 800 less than expected by experts. The company disappointed with lower than expected results and especially with the downward revision of its revenue figure for the last quarter of the year, its key moment of the year. For Bankinter analysts, “after explosive growth during the Covid-19 crisis, growth moderates and the group is subject to greater political scrutiny in the US and Europe. The performance of the advertising business and Amazon Web Services remains robust (+ 39% in the quarter), but that of online commerce (+ 3%) slows down and the group anticipates that it will continue to slow down and shows guidelines for Christmas below what is expected ”Of course, they trust its potential in the medium term. From Goldman Sachs they recommend buying Amazon although they lower the target price from $ 4,250 per share to $ 4,100, which still leaves a potential of 23%. “Although the stock could react negatively in the short term, it is one of the best options at one year with an increasingly positive bias in its risk-reward after 16 months rising less than the indices”, they conclude.

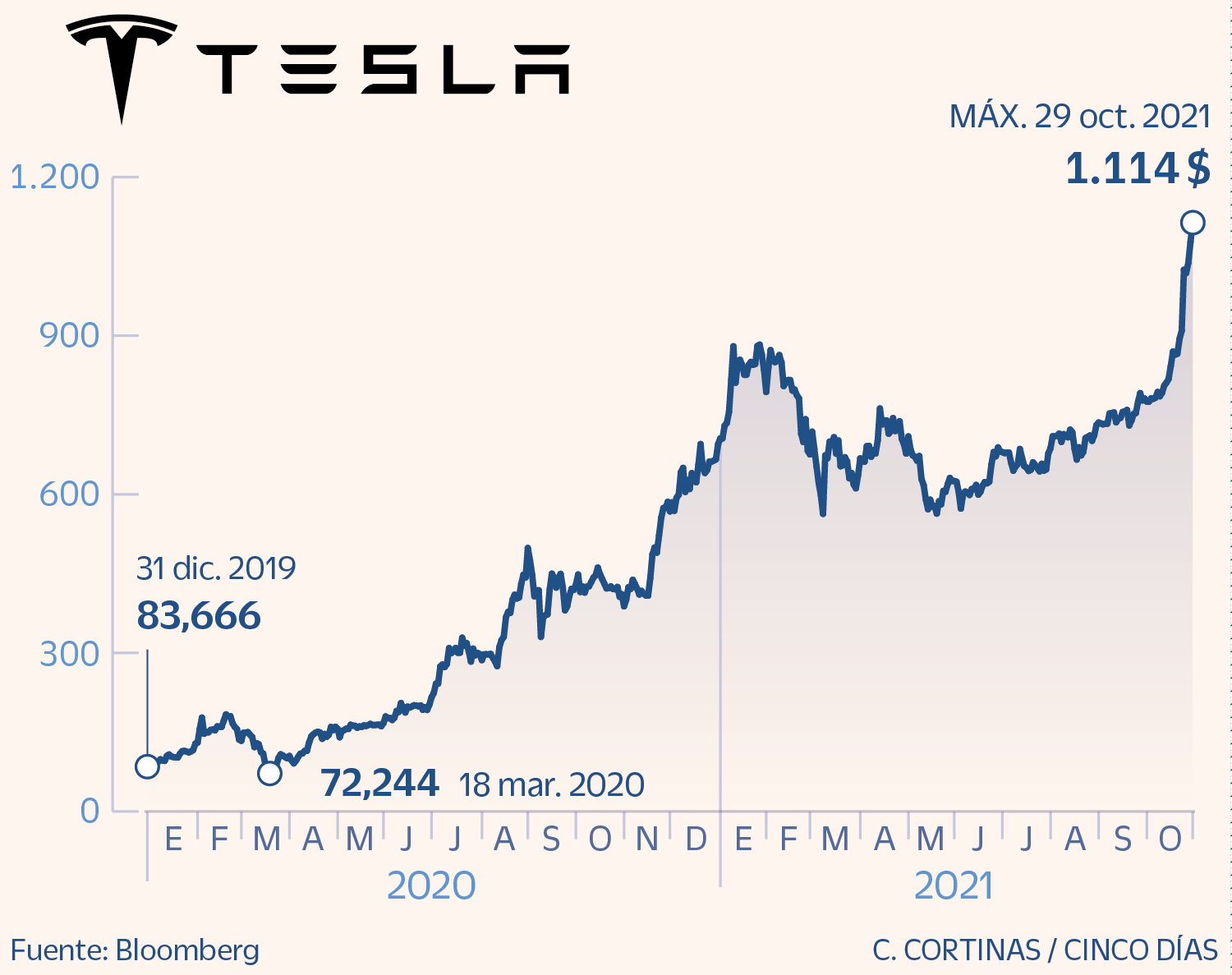

Tesla: Connects to Billionaires Group with Record Results

Is it possible that a company with a PER (number of times the price contains earnings per share) of almost 340 times is still a call option? Well, it seems that yes, that it is pure magic of its controversial creator Elon Musk. This week, just days after presenting its results, the electric car maker received the largest car order in history with 100,000 units from car rental firm Hertz. Order and results that, against the logic of the most conservative analysts, led the automotive giant to exceed the value of a trillion dollars on the stock market The firm earned 1,618 million dollars in the third quarter with a turnover of 13,757 million dollars . In addition, the Tesla Model 3 was also the best-selling car in Europe in the month of September. Of its results, Goldman Sachs only sees the energy division disappointing. “We maintain our buy rating on the shares and believe that Tesla’s automotive record this quarter is a positive indicator for future earnings potential,” they explain. From the independent analysis firm Zacks, located in Chicago, they note that “Tesla reported stellar production and deliveries in the third quarter of 2021 despite the global shortage of chips,” they indicate.

.

#trillion #dollar #companies #club #largest #economy #world