The upward streak of the Spanish economy continues, with GDP growth of 0.7% at the beginning of the year, more than double the European average. The foreign sector contributes almost 70% of this growth, the result of the boost in service exports and the slackness of imports, a factor that mechanically detracts from activity. The remaining 30% comes from domestic demand, this being a variable that also seems to evolve in a more balanced way: investment rebounds after the hit of the pandemic and global uncertainties, while the pull of public consumption dissipates. in a context of budget extension. And family consumption benefits from the rise in labor income.

To what extent does the Spanish economy have the resources to sustain a balanced expansionary cycle? Some signs are encouraging. Spain seems to have strengthened its international competitiveness thanks to access to abundant and cheap energy in relation to the main community partners; to the shortening of the supply chains of large corporations, in a logic of commercial blocks; and immigration, a plus for a productive model based on the incorporation of the workforce. However, the energy crisis and geopolitical tensions, clearly harmful in the short term, could have generated tectonic movements in globalization with surprising collateral effects for our economy.

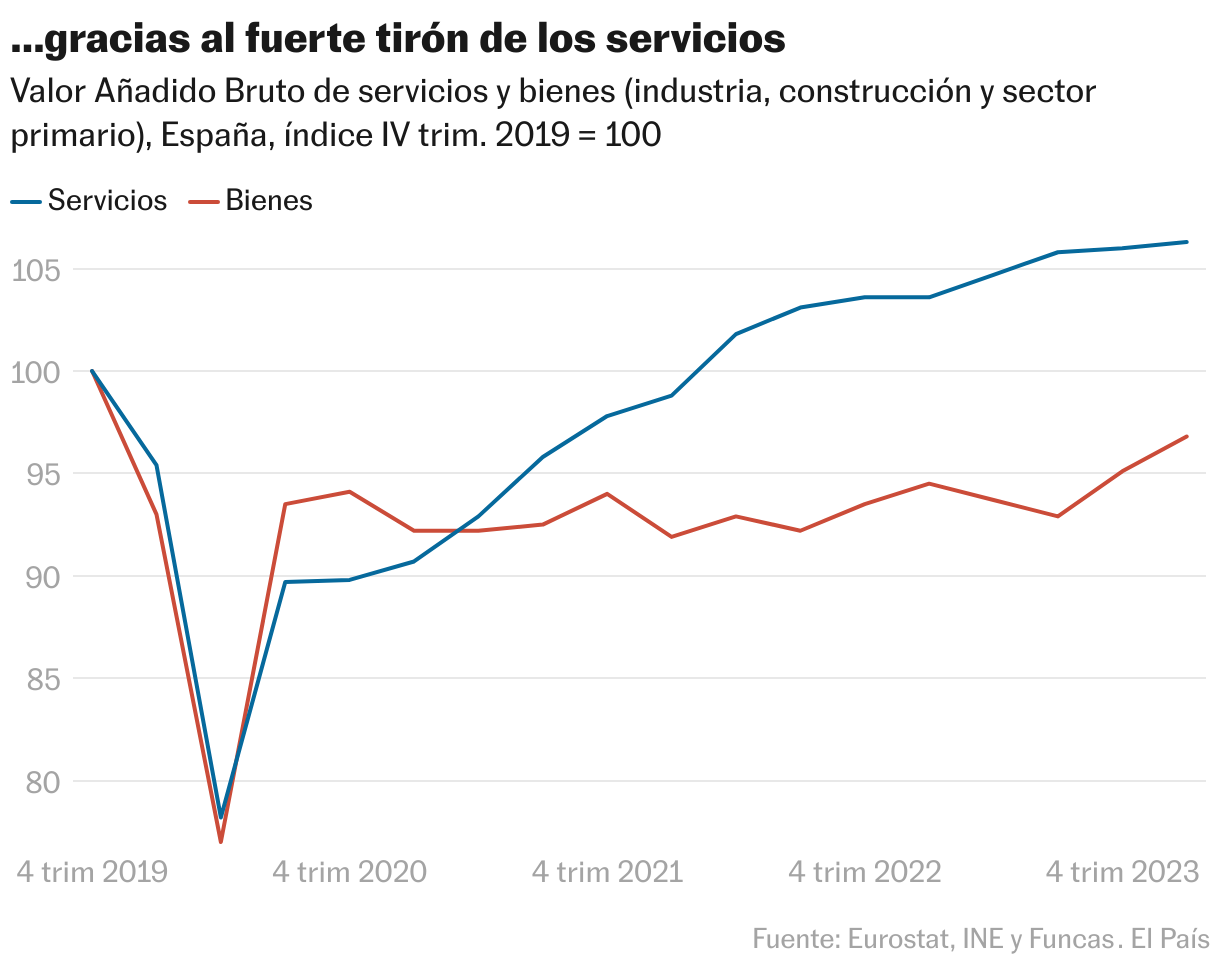

Faced with the hypothesis of a shock favorable supply, it is worth recognizing the role of volatile factors on the demand side, which will disappear sooner rather than later. Firstly, global consumption has temporarily shifted towards services – with our country being one of the main beneficiaries – to the detriment of goods, particularly industrial ones. According to Eurostat, compared to the pre-pandemic situation, European households spend proportionally more on travel, restaurants and other services, and less on industrial products, affected by supply problems and the energy crisis.

The deviation is perceived in the Spanish economy: the added value of the services sector was 6.3% above the pre-pandemic level in the first quarter, while the goods sector, which includes industry, construction and branches primaries, fell 3.2%. However, consumer preferences are set to normalize as relative prices stabilize.

Secondly, the weak performance of imports is a largely ephemeral phenomenon, since it reflects at least in part the shift in demand towards services, these being four times less intensive in imported inputs than goods (according to estimates based in tables input-output, supported by a recent ECB study). So it is foreseeable that imports will recover as consumer preferences are restored, even taking into account an eventual improvement in the share of Spanish companies in the domestic market.

The probable dilution of the changes in the pattern of demand, together with the restrictive turn in fiscal policy, will weaken the expansionary cycle, whose persistence will therefore depend on the persistence of the positive supply shock, that is, on our ability to promote structural advances in improving the production model. The turning point should occur next year, when less buoyant demand is anticipated as a result of the normalization of consumption patterns, both public and private. The key is to strengthen the current competitive advantages, with investment being a necessary condition to achieve this, particularly in a context of accelerated technological change. In this regard, the rebound in investment is still too incipient to envisage an expansion of productive capacity. And to unblock productivity, the key to generating an unprecedented, but achievable, cycle of sustainable convergence with Europe.

Investment

Investment (GFCF) rose 2.6% in the first quarter of 2024 thanks to the recovery of capital goods components and non-residential construction. Investment in housing and products of intellectual activity, however, fell. Despite the result achieved between January and March, investment is still 2.2% below the pre-pandemic level. The investment deficit in housing reaches 8.2%, and in the case of capital goods, 6.4%. Only investment in other constructions and intellectual property products exceed this level.

Follow all the information Economy and Business in Facebook and xor in our weekly newsletter

Subscribe to continue reading

Read without limits

_

#expansive #cycle #economy #expiration