The fixed mortgages cheap come to an end. The offer at competitive prices is vanishing due to the rise in interest rates and the incessant rise in the Euribor. Banks have totally changed their strategy and prefer to grant variable mortgages to obtain higher margins, so that they are making fixed rates more expensive at a forced march to discourage their contracting. So much so that the showcase has turned around in just days Y and only three entities offer fixed mortgages below 3% APR.

“Time is running out to get a fixed mortgage at a good price; banks have shot up the price of fixed mortgages in recent months,” they say from the financial comparator HelpMyCash.com. Last week, CaixaBank, the largest Spanish bank by volume of assets, raised its fixed mortgage above 4%, while in Abanca the linked interest already exceeds 5%.

“The evolution of rates is marking the future of the mortgage market. The change to positive of the Euribor means a new paradigm for the sector and those fixed mortgages of around 1% that could be seen at the beginning of this year can no longer be found. The fixed offers are less and less interesting for the new mortgagee”, assures Ferrán Font, director of studies at piso.com, who adds that the banking entities now prioritize and give better conditions in the variable mortgages “because the situation is completely different from that of the beginning of the year, with interest rates already around 2%”.

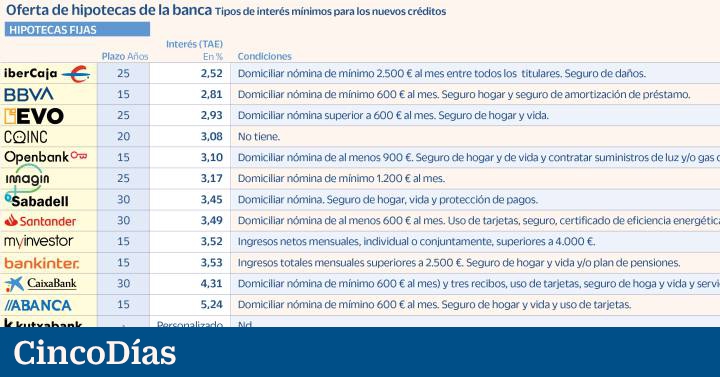

Specifically, at the moment, Ibercaja, BBVA and Evo Banco sell the cheapest fixed mortgages.

Ibercaja has several options depending on the client’s profile, but the most attractive is the Easy Mortgage at a fixed rate at 2.52% APR for amounts from 100,000 euros in exchange for direct debiting the payroll of the borrowers for a total amount of, at least, 2,500 euros. It is also necessary to take out damage insurance. Its other fixed-rate proposal, the Vamos Mortgage, also offers interest below 3%, 2.95% APR, but the link is more demanding.

In BBVA, the subsidized fixed rates remain below 3% APR, except in terms of up to 30 years (3.06% APR). The lowest interest rate is 2.81% APR for 15 years, provided that the client directs the payroll of at least 600 euros per month and takes out home and payment protection insurance. The application and process is digital. The entity has also launched the ‘Invite a Mortgage Friend Plan’, a promotion that allows customers to obtain 300 euros for each friend or family member who becomes a BBVA customer and takes out a mortgage within six months. The sponsor can bring up to a maximum of ten sponsored children who will also receive 300 euros each.

Evo Bank has recently made its fixed mortgage more expensive, which now has a price of 2.93% APR for 25 years. It is necessary to carry assets over 600 euros per month and take out home and life insurance.

According to an iAhorro study published last Thursday, in the last four months banks have implemented major changes in their mortgage products and average fixed rates have grown by 0.54%, while variables have fallen by 0.17% on average . Thus, cheap fixed mortgages, less than 2%, are now practically impossible to find.

Coinc offers 3.08% APR for 20 years without contracting any additional product, but the offer is for new customers and only for new mortgages that do not need guarantors or other guarantees. In open bank, the fixed interest is 3.10% APR for up to 15 years, fulfilling the conditions of payroll debit, home and life insurance and contracting electricity and gas supplies with Repsol. In case of financing more than 150,000 euros, the interest rate is reduced by 0.10%.

ImaginBank interest has risen 1% at once, from 2.17% to 3.17% APR. The only condition is to domicile the payroll from 1,200 euros per month. Of course, you have to apply for the mortgage from the application and the process is 100% online.

Sabadell Bank offer a fixed mortgage with an interest rate of 3.45% subsidized APR, direct debiting payroll and taking out home, life and payment protection insurance. The Bonus Fixed Mortgage of Santander Bank places the APR at 3.49%, fulfilling conditions: direct debit the payroll of at least 600 euros, use cards, take out some insurance and provide the energy efficiency certificate of the home with category A or B.

MyInvestor, Bankinter They offer very similar interests, 3.52% APR and 3.53% APR for a term of 15 years. The neobank only requires income, individually or jointly, of more than 4,000 euros per month. For its part, at Bankinter it is necessary to have recurring income of more than 2,500 euros per month, take out home and life insurance and make contributions to the pension plan.

For its part, CaixaBank The fixed mortgage has just been raised from 3.36% to 4.312% APR with a maximum bonus: direct payroll of at least 600 euros and three receipts, make purchases with cards, take out home and life insurance and alarm service. Abanca exceeds 5% APR with the maximum connection.

ENG, Kutxabank Y Unicaja Bank they personalize the fixed mortgage according to the client’s profile. On their respective websites there are simulators where you can check how the prices are depending on the amounts and the terms.

Sergio Carbajal, head of mortgages at Rastreator, stresses that “in the face of rising rates, entities find it increasingly difficult to offer competitive rates.” He clarifies, however, that this change in trend “is about something cyclical.”

In spite of everything, from HelpMyCash they assure that “there are still banks that offer attractive fixed mortgages and contracting a loan of this type is still a good option for clients who are looking for stability against the rise in the Euribor”. Of course, they insist that “it is convenient to close the contract as soon as possible” because the forecast is that the banks will continue to make their fixed mortgages more expensive given that the ECB is going to continue increasing the guiding rates.

In this context, a mortgage broker can help the client get the mortgage sooner, since it requests financing from several banks at the same time and saves time. “

Given that the situation is very volatile, it is best that those interested in a mortgage loan ask for help from advisers and experts who can help them at this vital moment, since there are many options in the mortgage market and analyze the small print and know what appropriate in each case is essential in order not to overpay”, points out Carbajal.

#decline #fixed #mortgages #banks #raise #prices #forced #pace #offers #fall #APR