Small savers have begun to react to the obvious profitability offered by Treasury bills, undoubtedly much higher than what they can aspire to in any bank deposit. The interest of individuals for this short-term public debt title has skyrocketed in the month of January. The last auction of one-year bills offered a return of 2.93%, an undeniable attraction compared to deposits that are remunerated almost at zero, even more so taking into account that the bills can be acquired from a minimum amount of 1,000 euros and without hardly any cost if they are purchased on the Treasury website or at the Bank of Spain offices.

As explained by financial sources, in the two bill auctions in January there has been non-competitive demand (corresponding to the acquisition on the Treasury website and in the Bank of Spain offices) for “several hundred million euros”.

The interest is also very palpable in the offices of financial institutions, where clients can request the purchase of bills, although in this case they will have to assume the intermediation commission charged by the bank, as in the purchase of shares. Sources from a large financial institution explain that the number of daily purchase operations of Treasury bills, either in private banks or in commercial banking offices, “has gone from a few to between 30 and 50 per day.”

The demand for Treasury bills by individuals already began to pick up clearly in October, once the rate hikes took Spanish sovereign debt as a whole out of negative profitability.

The demand from individuals already took a big leap in October, with the end of negative interest

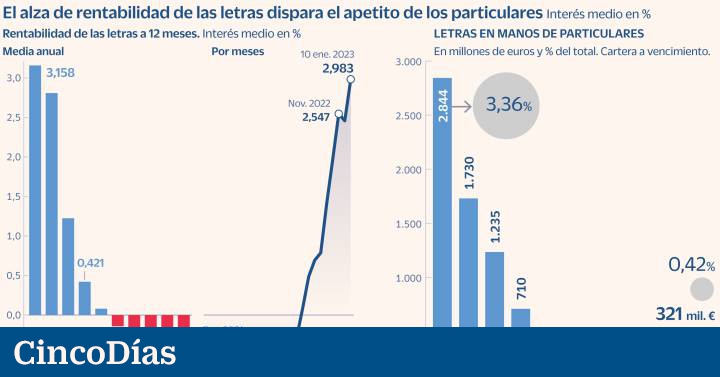

In August, negative State financing already disappeared completely, when the Treasury placed three-month bills with positive interest for the first time since 2014. And in October, the holding of Treasury bills in the hands of individuals had shot up to 321 million euros, from 99 million in September and in stark contrast with just 20 million of the monthly average of the last two years.

For the individual, there is currently no alternative in conservative savings that is more profitable than bills. Evidence that will add pressure to banks to start paying more for deposits, which barely earn more despite the sharp rise in interest rates. At a term of 12 months, the best offer is the 2.1% paid by Pibank, compared to almost 3% of the letters, and already at 18 months, the 2% APR of Wizink. Yes, there is more competition in payroll accounts. Bankinter pays 5% APR the first year for domiciling payroll in the entity –from a minimum of 800 euros per month– and CaixaBank has begun to offer 5% APR for two years for domiciling payrolls from 2,500 euros

rising demand

The volume of bills in the hands of individuals represents a tiny part of the total, only 0.42%. The one-year profitability of these titles has climbed to the highest level since 2012, in the midst of the sovereign debt crisis, when the volume in the hands of individuals was much higher: 2,844 million euros, 3.36% of the total. Financial sources explain that the demand for bills will increase in the coming months, not only among individuals but also among institutional investors, especially among fund managers. Short-term debt, from one to three years, is in fact used to create portfolios of funds such as guaranteed ones, for which they ensure a return to maturity with minimal management.

“Demand for bills has grown from different investor segments because they offer attractive returns,” says one of the Spanish Treasury market makers. In the nine-month bills auction on January 17, the second of the year, the demand exceeded the offer by 3.7 times and even so they were placed at an interest rate of 2.84%, an all-time high. In three-month bills, requests were almost four times higher than what was offered and the interest rate was at the highest level since 2012, at 2.198%, compared to 1.617% in the previous auction.

However, the increase in bill placements is not in the Treasury’s plans. Its financing plan for 2023 foresees a gross issuance of letters of 84,325 million euros, which will mean a decrease of 5.6% compared to what is issued in 2022. In addition, amortizations will once again exceed placements and net issuance this year it will be reduced by 5,000 million, in accordance with the objective of avoiding a decrease in the average life of sovereign debt.

#Private #individuals #trigger #demand #bills #Treasury #auctions

/cloudfront-eu-central-1.images.arcpublishing.com/prisa/N6X2XKYX2ZC7FP7LAG4T73XWSI.jpg)