Tech stocks from all corners of the world – from Asian stocks that experienced a ‘déjà vu’ of Black Monday in 1987 on Monday, to the untouchable Magnificent Seven – have been dyed red at the start of August, and after months of strong gains they are experiencing the bitter taste of declines. Until July 16, when the S&P 500 reached its all-time high, the index climbed 15% throughout the year. The Nasdaq, for its part, had risen 23%. Since then, they have lost almost 9% and 12% respectively in the bearish wave, and the Magnificent Seven lost 2.69 trillion in value on the stock market in the over the course of a month. From the Tokyo Stock Exchange to the New York Stock Exchange, risk aversion has revealed the shadows of the technology heavyweights.

Six of the Big Seven have already reported their earnings (Nvidia is missing), and investor confidence in artificial intelligence (AI) has begun to show some signs of weakness. Among the biggest concerns, analysts point to the sector’s overvaluation: the price-to-earnings ratio (PER) is 60.8 times for Nvidia and 34 times for Microsoft. However, the profits obtained by technology companies in the S&P 500 were only 0.15% higher in this last quarter. Such demanding valuations need to be justified by constantly growing financial data, but the results of the quarter open the door to more moderate returns. Exposure to the US macroeconomic environment and the investments required by the commitment to artificial intelligence have called these expectations into question. The bottlenecks in the world of chips, exemplified by the delay of the release of Nvidia’s ‘Blackwell’ AI processor by up to three months, are another turning point.

Technology is one of the most rate-sensitive sectors, and one of the most risk-exposed investments, which makes it placed in the crossfire of ‘Black Monday’The distrust generated by the latest employment data in the United States on Monday was the most opportune window to sell shares at the peak of their rally, and obtain profits from the most popular sector on Wall Street.

The panic on Monday sent the Philadelphia Semiconductor Index, the benchmark barometer for microprocessor manufacturers, down 15%. As for specific firms, the biggest losers were ASML (-14%), Lam Research Corp (-14%) and Nvidia (-9%), the only one of the Magnificent Seven to appear on the index. Taiwan Semiconductor Manufacturing Company (TSMC), the main supplier of these chips, was also among the hardest hit, and it spread to the Taiwanese stock market on Monday.

That said, although the sector’s grey areas have become more evident in the last 24 hours than in the last year, Monday’s slump has not yet influenced analysts: they remain confident in their bet. The outlook for the sector, according to UBS, remains “rosy” for the second half of 2024 and beyond. The entity sees a delay on the part of technology firms in proving the profitability of this bet as likely, but stresses: “There are no signs that companies are backing down on their investment plans, given the promise of this technology.”

The technological results of this semester have not impressed, and the firms of the ‘Big Tech‘ were already beginning to feel the first tremors of a correction after a series of disappointing results. A key trigger was the presentation of Amazon’s results, which failed to meet analysts’ forecasts last Thursday, and which have dragged the giant down by more than 11% in recent days. Amazon, however, continues to have the support of 93.5% of experts, even more than the darling of technology, Nvidia. Apple, one of the companies in the sector that has lost some of its shine in recent times, has presented results that Bank of America has described as “mediocre”. Even so, the analysis firm remains confident that sales will once again gain more momentum after the release of the iPhone 16.

The consensus among strategists at the largest Wall Street firms, from Deutsche Bank to Citi, is that technology companies will return to profitability in the second half of the year. Monday’s market rout only signaled a cooling of investor expectations, and the vast majority of analysts anticipate that this downward adjustment is short-term. “Markets also appear to have grown impatient for evidence that heavy investments in AI are beginning to bear fruit for major technology companies,” commented UBS.

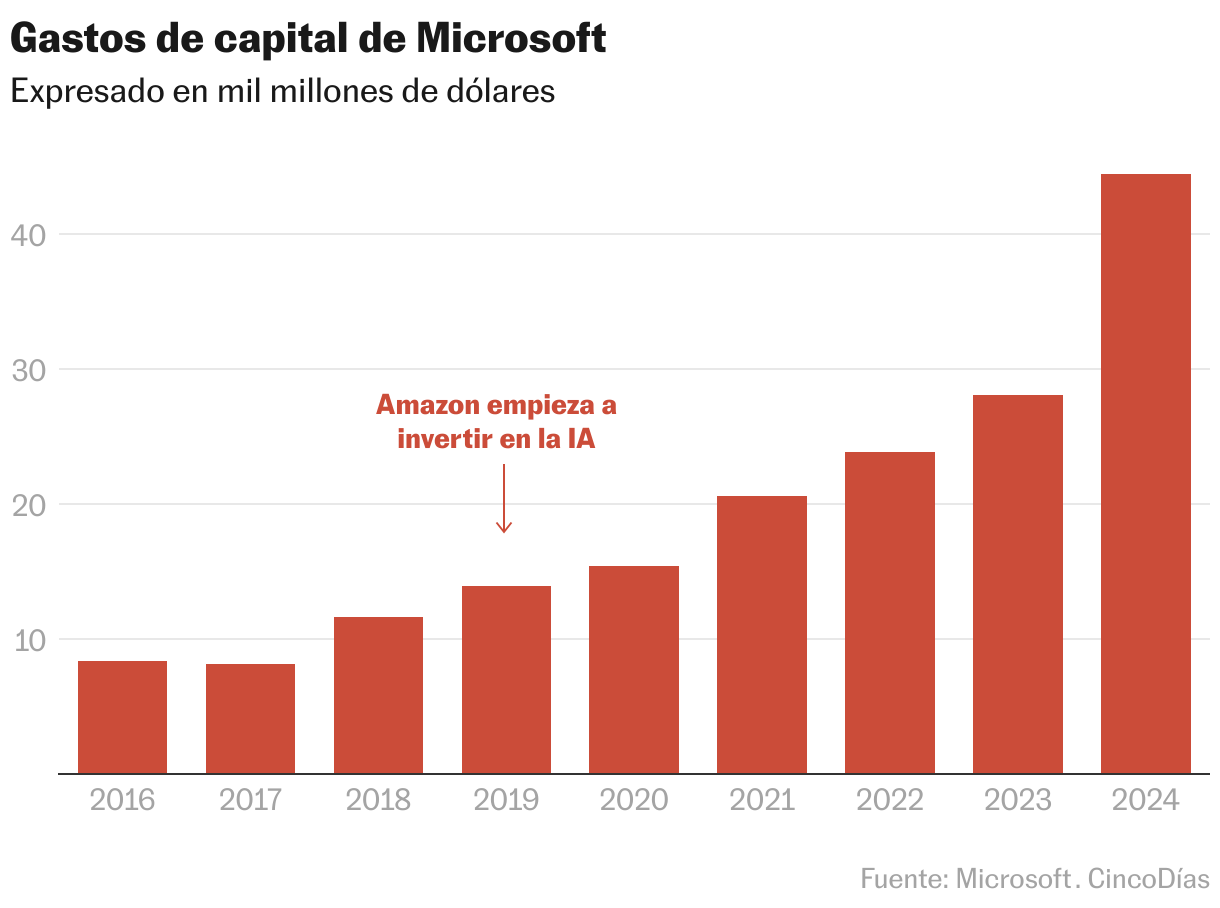

Betting on the potential of AI has become costly. One trend that has worried analysts has been the rise in capital expenditures each year by the largest technology companies. Investment in cloud infrastructure, i.e. data centres, is one factor that threatens to unbalance returns for investors: UBS anticipates that capital expenditures by the big tech companies will grow by 43% year-on-year, compared with the 24% expected in profits.

Microsoft acknowledged that almost all of its capital expenditures are allocated to AI and the cloud and that “about half of that is allocated to infrastructure as we continue to build data centers to support monetization over the next 15 years.” This is also the case for Meta, which has warned that it anticipates an increase in its capital expenditures by 2025.

So far, the market volatility has not led analysts to put a sell sign on any of the big tech stocks. Citi lowered its sales expectations for Blackwell by 5% for the next fiscal year, but continues to reiterate its 90% share of the AI GPU market, leaving Nvidia in a strong buy position. Goldman Sachs strategists are more optimistic and do not foresee a drop in sales for next year. Nvidia continues to retain a very favorable reputation from its analysts, at 87.8%, although this is not comparable to its rating almost unanimous a few months.

Deutsche Bank shares the general view. Indeed, analysts see it likely that “after the sharp fall in technology stocks, the valuation of the sector is starting to look more attractive again.” Deutsche Bank tends to favour European technology stocks over the Magnificent Seven, and sees more profitability in Dutch ASML, SAP and Capgemini. For Javier Molina, senior market analyst at eToro, the massive sell-off in technology stocks on Monday has reflected “the fragile and volatile nature of today’s markets.” Molina has advised investors to remain calm, reconsider their strategies and “make informed decisions on how to manage their portfolios.”

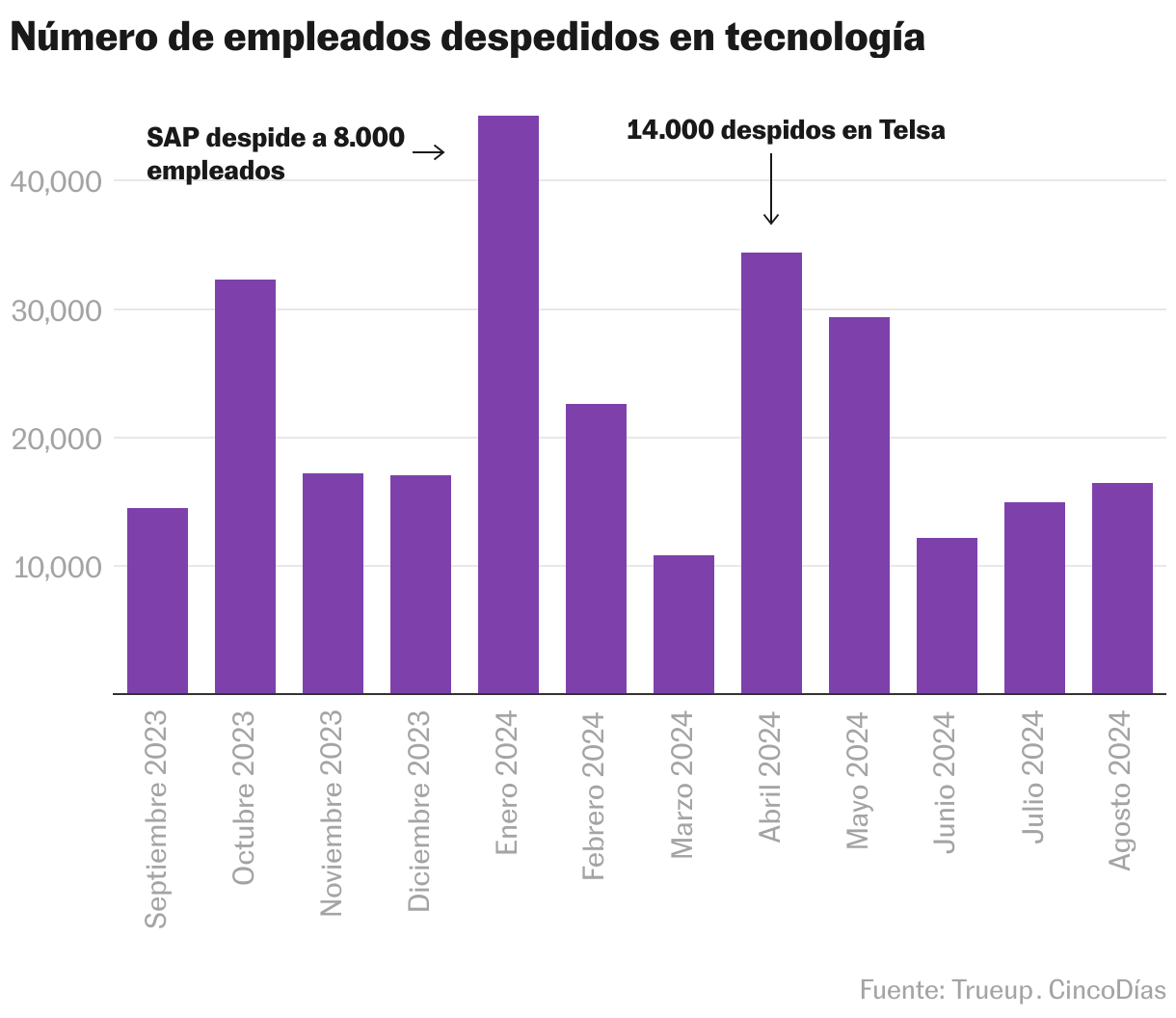

Another worrying trend within the sector is the wave of layoffs in the face of higher capital expenditure in this last quarter. Around 745 technology companies have laid off 185,867 employees since the end of 2023, according to the consultancy Trueup. The American chip manufacturer Intel led the stock market fall after announcing a layoff of 15% of its workforce last Thursday —15,000 workers— an announcement that was not well received by the market. This decision led Bank of America analysts to lower their forecasts for Intel to underweight, with a target price of 23 dollars (20 euros). It should be noted that Intel is an exception, it has been one of the players in the processor sector that has bet the least on AI. Microsoft, likewise, has laid off about 1,000 workers and has also been under scrutiny in recent weeks, after being responsible for a global computer blackout that brought airports around the world to a standstill.

Follow all the information of Five days in Facebook, X and Linkedinor in our newsletter Five Day Agenda

Newsletters

Sign up to receive exclusive economic information and the most relevant financial news for you

#Keys #weaknesses #big #tech #companies

{kind=link}