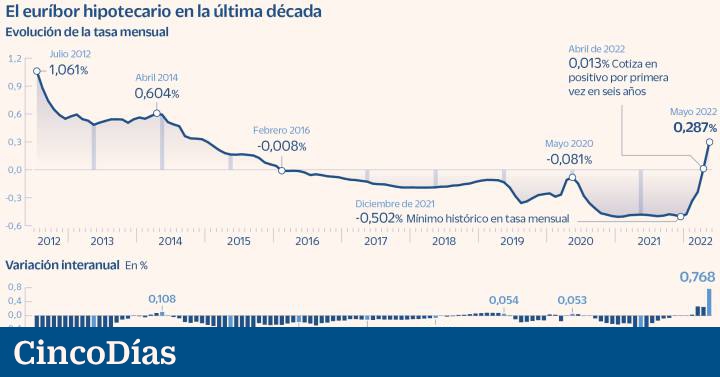

The mortgage market has experienced years of absolute deadlock, in which the prices of loans did nothing but get cheaper while the rise in interest rates seemed like it was never going to come. The panorama is now completely turning around and the mortgage Euribor has become explosively more expensive due to the rise in the price of money that is to come. An increase of 25 basic points in July that will be only the beginning of a process of increases that could leave them above 1.5% next year.

Bank customers have enjoyed extremely cheap mortgage loans in recent years, at least those who have the level of savings and income necessary to access a mortgage. The weighted average rate of new credit operations for home purchase has been below 2% continuously since 2015, according to data from the Bank of Spain. But between last December and April of this year it has increased from the minimum of 1.38% to 1.55%. And the rapid advance of the Euribor and the rise in ECB rates hopelessly predict more expensive mortgages from now on.

In the memory of thousands of mortgage holders there is still the rise in the Euribor of 2007 and 2008, when it exceeded 5% and triggered the monthly installment of loans. The rate reduction that began in 2008 left thousands of customers trapped and without the possibility of lowering their installments who had signed floor clauses without due transparency or information, a bad banking practice that is still going on in the courts.

However, that scandal was one of the great triggers for the new mortgage law, which came into force in June 2019 and which currently allows the contracting of mortgage loans with guarantees and transparency for the client. Thus, in the face of a new cycle for the mortgage market and interest rates, customers will have this time the guarantees of knowing what they are signing.

According to María Bueno, responsible for mortgage operations at iAhorro, “transparency has been improved in the granting of mortgages by banks, there are many more controls”. From the outset, the client will receive generic information about the mortgage loan from the financial institution, explaining issues such as the differences between fixed and variable rates and their implications; an example of the total amount of the credit, the cost for the holder, the total amount owed and the APR; a description of the conditions related to early repayment or an explanation of the consequences of not fulfilling the commitments associated with the credit agreement.

Contracting linked products is still a sensitive issue and mortgages still account for 35% of claims

Once this preliminary phase has been completed, the key to fully transparent information will be in the details of the binding offer that the bank presents to the client and that will allow them to compare between entities: amount, term, interest rate, commissions… It will include a document with simulations of the installments according to the evolution of the Euribor for variable-rate mortgages and clear information on the expenses that correspond to the bank –notary fees, registration, the cost of the agency and the tax on documented legal acts– and those that are borne by the client –the appraisal expenses and the simple note–.

In addition, a notary must certify that the client receives all the information and has properly understood it. Thus, in a first visit to the notary, chosen by the client, “the notary must check that all the documentation is correct and resolve the client’s doubts, but he must also make sure that he has understood all the details of the contract”, they explain from ENG. It will be the way to guarantee that, days later, at the time of signing the mortgage, the terms of the contract with the bank remain black on white.

“The mortgage reform has given legal certainty and peace of mind to customers that they contract the loan in the best possible conditions of transparency,” defends Santos González, president of the Spanish Mortgage Association. Even so, mortgages are the main focus of customer claims before the Bank of Spain. They represent 35.6% of total complaints, followed by cards, with 28%, according to the latest data from the regulator, from September 2021.

linked products

In the opinion of Asufin (Association of Financial Users), there are still some chiaroscuro in terms of transparency in the contracting of mortgages, the most sensitive of them being related products that allow improving credit conditions. According to its president, Patricia Suárez, “there is greater transparency in banking, things work reasonably well, although the mortgage law left the door ajar with the issue of linked products.”

Thus, it establishes that the only product that the client is obliged to contract is home damage insurance and determines that the entity must present the client with a mortgage offer without other related products. In short, you cannot force the contracting of additional products for the granting of credit. Although, according to Suárez, the reality results in many occasions in which the client agrees to subscribe to other products –pension plan or life insurance– to obtain the granting of the credit.

The duration of the bank’s binding offer has been reduced from months to weeks

In addition, the entities are not obliged to specify the effective savings that the contracting of other products supposes in the mortgage. It is enough, for example, to quantify it as a reduction of 10 or 20 basic points on the interest rate. It is not necessary, according to Suárez, to quantify in euros the annual savings that this may entail. “The law is limited to stating that the bank must explain the savings, but not how. For the consumer, calculating it effectively can be an effort. It is about making accounts: how much you save on the mortgage, for example, by linking a life insurance or if it could be more interesting in any case to contract it in another entity, ”he points out.

From the Spanish Mortgage Association, Santos González explains that “the client is not obliged to contract linked products. And if there are any, they will be clearly explained, with the possibility of contracting them outside the mortgage”.

fixed or variable

Once the transparency requirements and protocols have been fulfilled, the great dilemma that the client who is going to sign a mortgage now faces is whether to contract a fixed or variable interest rate. During the long period of interest rates at zero and even negative, banks have emphasized the marketing of fixed-rate mortgages, with rates higher than the variable ones that could ensure a little more margin, although the tough competition between entities has come to leave really attractive offers, less than 2% for a fixed rate. More than 70% of the new mortgage production is made at a fixed rate, a percentage that has reached maximums this year, according to INE data.

Faced with the rate hike that is coming, and which is already anticipated by the Euribor, financial institutions are recovering variable-rate mortgages in their shop windows, where competition and price wars are now concentrated and in which there is the opportunity to scratch more business margin in the future. “The offer at a variable rate and at a fixed rate will tend to balance out. Whoever wants the peace of mind of a fixed interest rate on the mortgage in the new market environment is going to find more expensive prices. For variable rates, the prices of the last six years have been a luxury”, adds Santos González.

From iAhorro, María Bueno points out that “banks are now directing their offer towards variable-rate mortgages.” Fixed-rate mortgages, especially attractive now before the ECB begins to effectively raise the price of money, “are being reserved for high-income customer profiles, in which the entity can obtain more profitability with other more affordable products. beyond the mortgage”, he adds.

Bueno also points out a new factor, together with rising rates, which is appearing in the mortgage offer of Spanish financial institutions: the shorter duration of the binding offers they present to their clients. “If before they could be valid for six months, now they can be only two weeks. The market changes every day. The client has to decide quickly. And if he is clear about it, it is better not to wait”, he concludes.

The endless lawsuit of the floor clauses

Macro demand. The marketing of mortgages with floor clauses continues to kick in the courts. The Adicae association demands the return of 190 million euros in a macro-cause that it initiated against 101 entities and on which the Supreme has yet to rule. The high court considers that it could be pertinent to transfer it to the CJEU, for which it has consulted with the parties. If it goes to the instances of the European justice, the resolution of the case could take two more years, eternalizing a process that dates back to 2006 and 2007, in which the inclusion of floor clauses before the start of the lowering of interest rates was common practice in banking. So far, the courts have overwhelmingly agreed with the plaintiffs, with 97% of rulings favorable to the return of the overcharge.

#Keys #cover #mortgage #face #rising #rates