FACE TO FACE For Marciano Testa (right) and Glauber Correa, chairman and CEO of Agi, it pays to take people out of the “call centers” and put them face to face with customers. (Credit: Rafael Cusato)

Advertising campaigns for financial apps often show young customers comfortable with their smartphone technology. This image does not always correspond to the reality of the Brazilian market, which is characterized by low-income and increasingly younger customers.

The former CEO and current chairman of the Board of Directors of Agi, Marciano Testa, is well aware of this. “Our priority market niche is among customers over 50 years old and with an income of around R$ 4 thousand per month”, said Testa. That’s why Agi’s activities, founded around 20 years ago in Porto Alegre, go against the grain of fintechs. In the 12 months ending in September 2021, the financial institution did something unthinkable for today’s Brazilian bankers: it opened 208 branches.

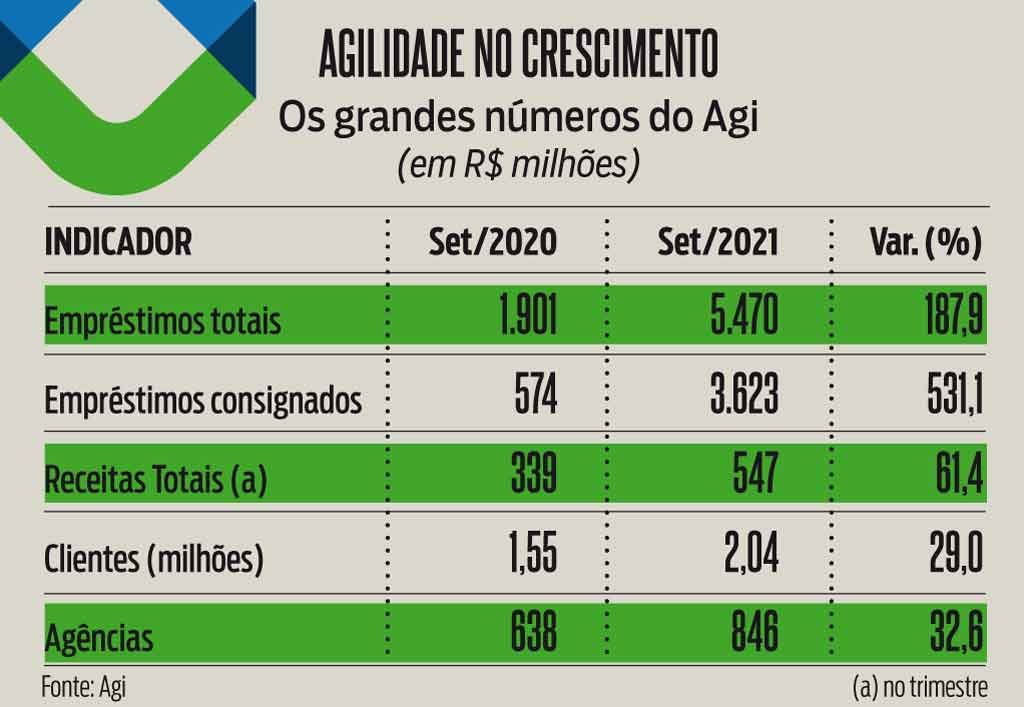

Agi’s physical network grew 32.6% and, at the end of the third quarter of last year, had 846 addresses. The units are called smart hubs by Agi. “They don’t have revolving doors, they don’t use paper and they don’t move money,” Testa said. Even so, its function is the same as traditional bank branches.

According to Glauber Correa, who succeeded Testa as CEO of Agi, the explanation is simple. Mature customers are less familiar with the technology. It is common for them to need assistance when downloading and configuring applications, in addition to learning how to carry out financial transactions in the digital universe.

That’s where the agencies come in. They are dry spaces, with a self-service totem and three employees on average. They help in the digital journey and, on top of that, take advantage of the contact to sell products and services. “Instead of doing like many fintechs and leaving professionals in call centers, our employees are present to serve customers,” said Correa.

CONSIGNED It ensures that the investment pays off. On average, he said, the customer who comes to terms with the technology in the sixth interaction with the bank’s professionals. “From there, ‘cross-selling’ increases exponentially,” said Correa. And, on top of that, it facilitates customer interactions with family and friends, something essential in this income bracket. Not by chance, most of the credit granted by Agi is payroll-deductible loans. At the end of the third quarter, the bank had a loan portfolio of BRL 5.47 billion, a growth of 187.9% compared to the same period in 2020. Of this total, BRL 3.62 billion, or 66%, was of payroll loans. In this period, the total number of customers increased by 29%, growing from 1.55 million to just over 2 million.

As a result, revenue for the third quarter of last year rose 61% compared to 2020, reaching R$ 547 million. However, the bank suffered an unadjusted net loss of R$42.4 million in the third quarter, after having made a profit of R$32 million in the same period last year. In the first nine months of 2021, the loss was BRL 14.8 million, compared to a profit of BRL 70.7 million between January and September 2020.

The growth strategy has been going through some route corrections. At the end of 2020, Agi transformed its technology department into a company, Hypeflame, and placed it under the responsibility of Fernando Castro, a career employee at Sicredi and who was in charge of Agi’s technology. The spin off started big, with 100 employees, and reached 400 at the end of last year, when several people were laid off and activities were reduced. “We’ve always been a self-sustaining business, we never thought about burning cash for several years in order to be profitable,” Testa said.

Despite appearing to be against the market, with its physical proximity, Agi obtains more customer loyalty, especially those over 50 years of age, who still insist on face-to-face contact. And that can make a difference at a time when the retraction of international liquidity makes life more difficult for fintechs 100% based on virtual transactions.

#Antifintech #Banco #Agi #born #startup #migrates #model #physical #stores #older #audiences #ISTOÉ #DINHEIRO