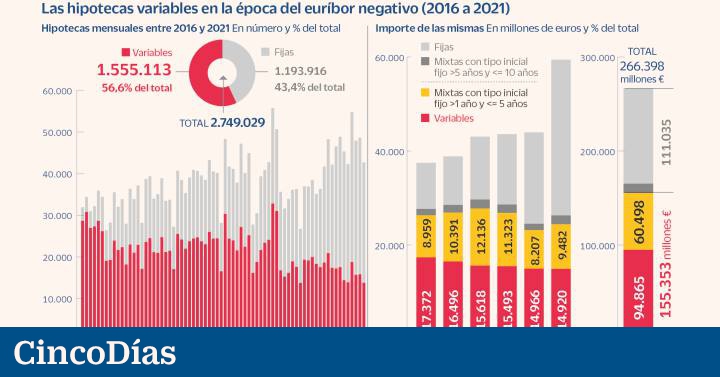

Slightly more than a million and a half variable mortgages signed between 2016 and 2021, with rates at zero, are the most affected by the rise in the Euribor and those that arouse the greatest concern in banks, which focus on vulnerable households with a high financial burden where defaults may arise.

These mortgages have barely paid interest so far. But the rapid rise in the reference index, which is already close to 3%, has triggered the installments of a loan portfolio that totals just over 155,000 million euros of outstanding mortgage balance. The bank sees a part of that amount threatened by the foreseeable rise in delinquency in the coming months.

Concern within the sector is focused on groups in vulnerable situations with more difficulties in meeting mortgage debt payments, according to financial sources, which point out, however, that it is a small group. For its part, the government believes that there are also middle-class families at risk. Precisely, delimiting who is vulnerable is one of the main stumbling blocks in the negotiations that bank employers and the Economy maintain to protect those mortgaged from the Euribor arreón.

The Bank of Spain has already warned of the rapid increase in the Euribor in its latest financial report, where it points out that families considered highly indebted, for allocating more than 40% of their income to debts, now rise to 14%. The percentage reaches 35% in the case of households with lower income. Experts recommend that the payment of the mortgage and the total loans not exceed 30%-35% of the monthly salary.

Bearing in mind that the 12-month Euribor reached lows of -0.5%, those mortgaged at a variable rate with differentials of 1% or less have enjoyed several years of low – or even zero – cost of financing. However, with the indicator hovering around 2.8%, the bill has risen considerably. In an average credit of 150,000 euros at 25 years that has to be reviewed, the monthly bill will go from 532 euros to 775 euros. It means paying 243 euros more per month or 2,900 euros more per year.

The impact of the Euribor is less on old mortgages, since most of the interest has already been amortized. But those formalized in recent years are still in the initial period, when the interest burden is higher, and they are the ones that will suffer the most from the rise in rates, testing the payment capacity of many families.

The president of the Spanish Mortgage Association, Santos González, points out that “the concern is shared and that is why there are ongoing negotiations to establish measures aimed at alleviating vulnerable groups.” He stresses, yes, that “there is no sectoral danger because the banks are highly capitalized and only a part of the credits will be affected.” He calculates that 10% of that 155,000 million mortgage balance could be compromised. According to recent data from the European Banking Authority (EBA), 15% of mortgage credit in Spain is sensitive to interest rate rises. The Spanish Banking Association (AEB) does not see a problem “for the moment” because the situation is very different from that of the 2012 crisis.

For Marta Alberni, consultant for International Financial Analysts (Afi), the percentage of vulnerable and delinquent households may increase in the coming quarters. “It is one of the challenges for the banking sector,” she says. But, as he explains, at the same time “there are two mitigating levers that play in favor of the banks: the largest contracting of fixed-rate mortgages since the pandemic and that the levels of indebtedness are much lower than those of the 2008 crisis” .

Experts point out that more than half of the mortgages have a percentage of financing on the appraised value, known as loan to value or LTV, of less than 80%, a threshold from which the credit granted carries more risk of non-payment.

Protection measures

Homes at risk. Banking and Government are looking for how to protect mortgages in the current context. The head of Economy, Nadia Calviño, advocates expanding aid to the middle classes. The Bank of Spain believes that the measures should focus on lower-income households and, moreover, be of a temporary nature. The sector defends that the mortgage is the last thing that the Spanish stop paying. The deal, which may include extending the term of the mortgages without increasing total interest, is expected to close shortly.

Moderate impact. Those responsible for the main banks agree that the rise in interest on the Euribor will have a moderate impact. According to Onur Genç, CEO of BBVA, “mortgages in Spain are not going to be an excessively serious problem. The increase in installments has a direct correlation with the date on which they were signed and in the last five years most have been at a fixed rate”. César González-Bueno, CEO of Sabadell, points out that from 2016 until now, 75% of the book is at a fixed rate.

#million #variable #mortgages #focus #banks #Euribor